BIL INVESTMENT INSIGHTS

Market Snapshot

The ongoing conflict in the Middle East continued to push oil prices higher last week, with Brent crude briefly rising to $106 per barrel. Prices continued to rise despite the International Energy Agency’s announcement of a record release of 400 million barrels from its strategic reserves to mitigate the impact of the disruption of the flows through the Strait of Hormuz, as persistent tension continued to dominate headlines.

With several major central banks scheduled to meet to discuss monetary policy this week, market participants are trying to assess the potential impact of elevated energy prices on inflation dynamics and, consequently, monetary policy decisions. The geopolitical escalation has already pushed inflation expectations higher, particularly in the US and Europe, as energy‑driven price pressures feed into market pricing. Rising oil and gas prices have contributed to higher government bond yields, with increases across US Treasuries, European sovereign debt, and UK gilts as investors reassess the likelihood of near‑term rate cuts. Given the uncertainty surrounding the duration of the conflict and its economic impact, most central banks, including the Fed and the ECB, are expected to keep policy unchanged this week while continuing monitoring developments.

Equity markets remain under pressure as investors grapple with geopolitical uncertainty, rising yields, and the potential for more persistent inflation.

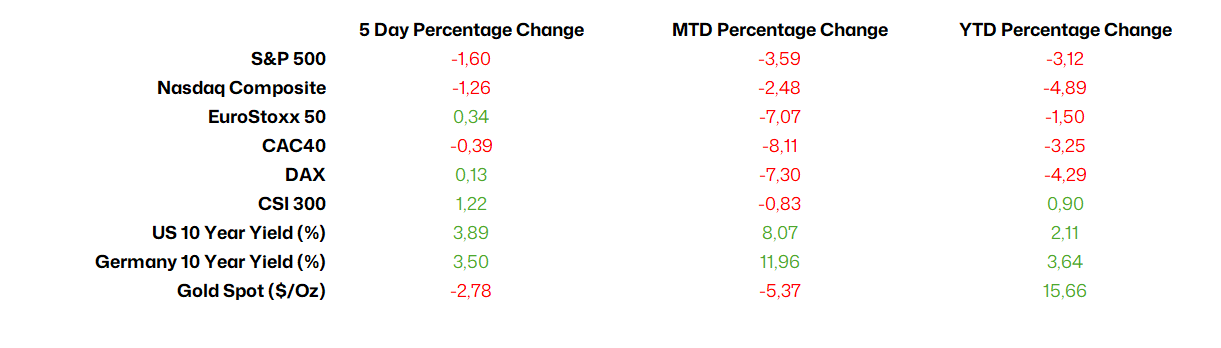

Source: Bloomberg, BIL as of March 16

Macro Snapshot

US Q4 2025 growth revised down to 0.7%

According to revised figures, the US economy grew by just 0.7% year on year in the final quarter of 2025, as exports, consumer spending and investment were lower than initially estimated. The GDP growth rate was sharply revised down from an initial estimate of 1.4%, slowing from the 4.4% growth rate seen in Q3. This suggests that the US economy weakened more than expected at the end of the year.

The Bureau of Economic Analysis stated that the net trade figure decreased due to a downward revision of services exports. Consumer spending on services was also lower than previously thought.

Much of the slowdown has been attributed to the federal government shutdown, the impact of which was also greater than initially thought. The recovery from the shutdown is expected to boost GDP growth at the start of 2026.

US inflation steady prior to Middle East conflict

US headline CPI inflation held at 2.4% year‑on‑year in the month preceding President Trump’s conflict with Iran. From here, however, tariff costs are expected to lift inflation in the months ahead, while the escalation in the Middle East also raises concerns about renewed price pressures stemming from rising energy costs.

Digging into February’s print, energy inflation firmed (0.5% vs –0.1% previously), driven by a smaller decline in gasoline prices (–5.6% vs –7.5%) and notable increases in fuel oil (6.2% vs –4.2%) and natural gas (10.9% vs 9.8%).

In contrast, prices for used cars and trucks fell further (–3.2% vs –2%), while food (3.1%) and shelter (3%) inflation remained unchanged.

Jewellery was a notable gainer, rising 11.2% year‑on‑year — a small‑scale reflection of broader geopolitical tensions. The increase has been fuelled by strong rallies in gold and silver, which typically serve as safe‑haven assets during periods of uncertainty. Over the past year, that uncertainty has been plentiful, first with tariff‑related disruptions and now with an escalating conflict in the Middle East.

On a monthly basis, CPI rose 0.3%, slightly above January’s 0.2%, matching expectations. Shelter contributed most to the increase, rising 0.2%, while gasoline climbed 0.8% and food prices increased 0.4%.

Core inflation — excluding food and energy — was stable at 2.5%, its lowest since 2021.

The report arrived just ahead of next week’s Federal Reserve meeting, where policymakers are widely expected to keep rates unchanged at 3.5%–3.75%. The recent surge in energy prices has led traders to scale back expectations for rate cuts this year. Markets are now pricing in only one or two quarter‑point cuts, compared with the two or three anticipated before the conflict broke out.

China’s export strength continues to prevail

China’s trade surplus widened to USD 213.6 billion in the first two months of the year, as exports surged 21.8% year‑on‑year - a sharp acceleration from December’s 6.6% increase and far above expectations. The January–February figures are combined to smooth distortions linked to Lunar New Year shifts. This marked the fastest export growth since October 2021, supported by robust global demand which is likely to continue into March as factories frontload shipments to the US during the temporary period of lower tariffs of 10% following the Supreme Court’s ruling that previous levies were illegal. The conflict in the Middle East, and the resulting energy supply disruptions, is a risk and could derail manufacturing activity in the months ahead. However, China has stockpiled key commodities needed by manufacturers at the start of the year, including iron ore and crude oil, and is relatively well-positioned for such supply disruptions.

Imports also rose strongly, jumping 19.8% amid firmer domestic demand during the festive season. Bilateral trade with the US, however, weakened: exports to the US fell 11%, while imports from the US dropped 26.7%.

China’s strong export performance at the start of the year will likely draw heightened scrutiny as Presidents Donald Trump and Xi Jinping are set to meet in Beijing at the end of this month. Several of China’s trading partners, including the US, have raised concerns that their markets are being flooded with low‑cost Chinese goods, putting domestic industries at risk. Yet the concurrent rise in imports may be viewed as a positive sign that China’s trade balance could become slightly less one‑sided. Although Beijing has pledged to prioritise boosting household consumption in 2026, activity at the start of the year was likely lifted by holiday spending and precautionary crude‑oil purchases ahead of the escalation in the Middle East. Stronger‑than‑expected data may also give policymakers reason to delay additional stimulus measures, particularly if consumption continues to hold up better than anticipated.

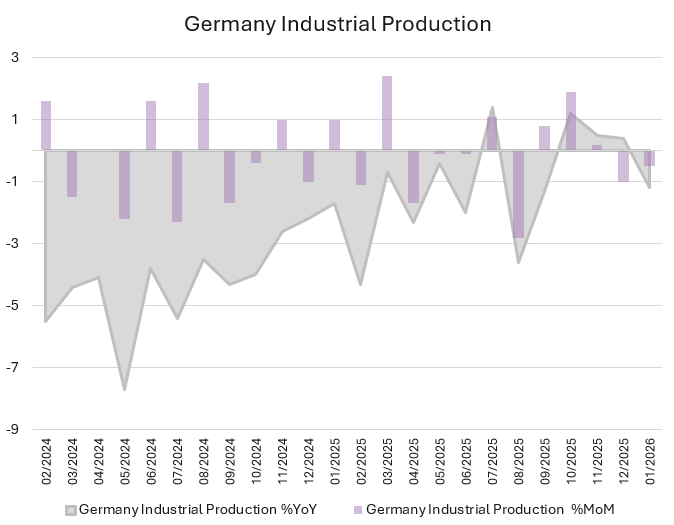

Germany industrial production stuck in the mud

German fiscal spending plans and improving soft indicators have recently fuelled optimism about an industrial turnaround. The Manufacturing PMI, for example, moved into expansion territory in February for the first time since June 2022, and the IFO index reached its highest level since August 2025, with a leg-up from better expectations for industry. In practice, however, the hard data is yet to show any meaningful industrial upturn.

Industrial output in Germany fell 0.5% MoM in January, following a downwardly revised 1.0% decline the month before, against market expectations of a 0.9% increase. This marks a second consecutive monthly contraction. The largest drags came from fabricated metal products (‑12.4%), pharmaceuticals (‑11.9%), and computer, electronic and optical products (‑6.8%). These declines were only partially offset by a 10.3% rise in energy production, reflecting colder weather, and by a 2.9% increase in construction output. Excluding energy and construction, industrial production fell 2.5%, with broad‑based weakness across consumer goods (‑4.2%), intermediate goods (‑2.6%), and capital goods (‑1.6%).

The persistence of weak output suggests that Germany’s industrial malaise is driven more by structural constraints than by short‑term cyclical forces—especially notable given that global industry is showing clearer signs of recovery. By comparison, French industrial production edged up 0.5% in January, and US manufacturing is gaining momentum with increasingly broad‑based improvements across industry groups.

The Bundesbank expects Germany’s expansionary fiscal stance to support growth more meaningfully only later in the year, and while defence and infrastructure spending should substantially raise government demand, it will have only a limited effect on Germany’s underlying productive capacity. The Bundesbank highlights the need for more comprehensive structural reforms to strengthen the economy sustainably.

Source: Bloomberg, BIL

Calendar for the week ahead

Monday – China House Price Index (February), Industrial Production (Jan-Feb), Retail Sales (Jan-Feb), Fixed Asset Investments (Jan-Feb), Unemployment Rate (February). US Industrial Production (February).

Tuesday – Eurozone & Germany ZEW Economic Sentiment (March). US NAHB Housing Market Index (March).

Wednesday – Japan Balance of Trade (February). Switzerland SECO Economic Forecasts. Eurozone Inflation Rate (Final, February). US PPI (February), Factory Orders (January), Fed Interest Rate Decision & Economic Projections.

Thursday – Bank of Japan Interest Rate Decision. Switzerland Balance of Trade (February). UK Unemployment Rate (January). Swiss National Bank Interest Rate Decision. Bank of England Interest Rate Decision. US Jobless Claims, Housing Stats (January). ECB Interest Rate Decision.

Friday – Eurozone Balance of Trade (January).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

April 27, 2026

Weekly Investment Insights

Market Snapshot US equities continued their strong performance last week, with several major indices reaching record highs, as broadly positive economic data and upbeat earnings...

April 20, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot On Friday, equity markets celebrated the opening of the Strait of Hormuz to commercial shipping during the ceasefire. US equity markets posted strong...

April 13, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Last week, oil prices slumped and equities rallied after the US and Iran agreed a two-week ceasefire. However, hopes for de-escalation were quickly...

April 13, 2026

BILBoardBILBoard April 2026 – Through the noise

Based on the Asset Allocation Committee on March 31 2026 Geopolitical uncertainty took centre stage in March as the conflict in the Middle East extended...