BIL INVESTMENT INSIGHTS

Market Snapshot

On Friday, equity markets celebrated the opening of the Strait of Hormuz to commercial shipping during the ceasefire. US equity markets posted strong gains with major indices reaching new highs amid signs of de-escalation of the conflict in the Middle East and some upbeat earnings results. In Europe, major indices also ended the week in green as optimism grew that the conflict could be nearing an end.

Brent crude prices fell to around $90 per barrel following Iran’s foreign minister announcement on Friday that the Strait of Hormuz was “completely open” to commercial shipping. However, volatility in oil markets persisted on Monday, with prices jumping after the US Navy seized an Iranian vessel accused of breaching its naval blockade of the Strait.

Despite last week’s optimism, it remains unclear whether new peace talks are set to begin. Washington and Tehran have issued conflicting statements: while the US has indicated that talks could start this week, Iran has denied this, citing ongoing US restrictions on Iranian ports.

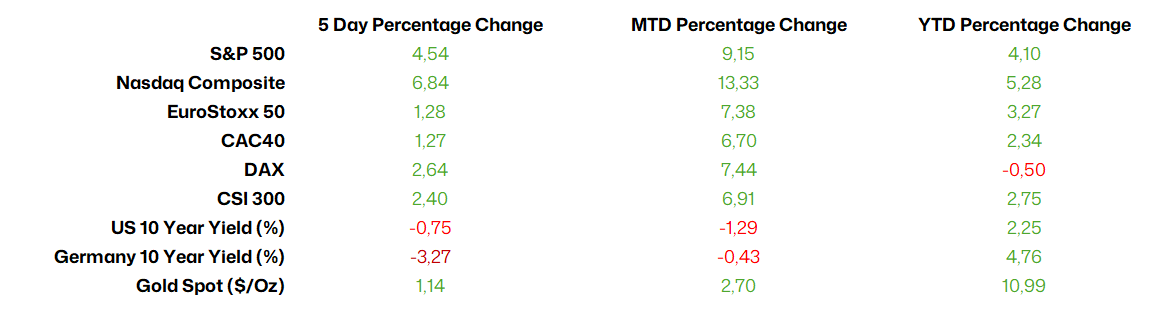

Source: Bloomberg, BIL as of April 20

Macro Snapshot

IMF cuts global growth forecasts amid Middle East conflict

The International Monetary Fund (IMF) last week warned that the global economy is at risk of growing at the slowest pace since the pandemic if oil prices remain at $100 per barrel for the rest of the year. The IMF predicts the global economy to grow by just 2.5% in 2026, and inflation to soar by 5.4%, in an “adverse scenario” in which the conflict in the Middle East causes oil prices to remain at their current level throughout the year. In a “severe” scenario, growth could slow to as little as 2% and inflation could rise to 5.8%. While the fund’s baseline scenario forecast growth of 3.1% this year and inflation of 4.4%, the projections were prepared before the recent ceasefire talks failed and assume a swift end to the conflict, with oil prices returning to around pre-crisis levels. With the latest developments in mind, the IMF hinted that their “adverse scenario” is becoming increasingly realistic.

Chinese economy grows by 5% in Q1

China’s export strength pushed economic growth higher in the first quarter of the year, with GDP growth accelerating to 5% year on year, up from 4.5% in the previous quarter. Increased domestic demand during the Lunar New Year holiday also helped push growth higher. The Chinese economy has, so far, managed to absorb most of the shock from the conflict in the Middle East thanks to significant oil reserves, a diversified energy mix, and state controls to contain price volatility. However, underlying momentum in the economy continues to be uneven, with industrial output growing more than expected in March, while retail sales missed expectations.

Factory output grew by 5.7% YoY in March, slowing from the 6.3% rise in the combined January-February period, but above expectations of a 5.5% rise. Activity was hit by the war in the Middle East, with activity moderating across the major sectors such as mining, manufacturing, and utilities, electricity, heat, gas, and water. Meanwhile, retail sales activity slowed to 1.7% YoY, down from 2.8% in the previous period as consumers slowed their spending following the Lunar New Year holiday earlier this year.

Despite the strong start to the year, rising energy prices stemming from the conflict in the Middle East are expected to begin weighing on the Chinese economy. While higher costs are likely to further suppress domestic demand, they may simultaneously support demand for China’s green-technology exports. As a result, the growing divergence between externally driven growth and weak domestic activity is likely to become even more pronounced.

Chinese exports slow amid Middle East turbulence

China’s trade surplus narrowed in March to its smallest level since February 2025, as export growth slowed sharply while imports surged. Exports rose 2.5% year on year, a significant deceleration from the 39.6% surge recorded during the combined January–February period. While a moderation was widely expected following the Lunar New Year distortions earlier in the year, the slowdown was more pronounced than analysts had anticipated.

One notable exception was refined oil products, exports of which rose 20.5% month on month. The increase reflects elevated energy market pressures from the ongoing conflict in the Middle East, which has boosted global demand for refined fuels.

Imports, meanwhile, expanded strongly, rising 27.8% year on year, well above expectations and accelerating from 19.8% growth in the previous period. The surge was largely driven by higher demand for technology sector-related inputs such as chips.

Exports played a central role in supporting China’s economic growth last year and are expected to remain a key pillar in 2026, despite official commitments to strengthen domestic consumption as well. However, as the effects of Middle East instability begin to filter through global inflation and economic activity, China’s export-led growth model may face increasing headwinds. Higher energy prices are squeezing household purchasing power worldwide, making consumers more price sensitive. As a result, Chinese manufacturers may struggle to pass on rising input and energy costs to end consumers without damaging demand.

Despite the near-term slowdown, China’s exports are expected to remain resilient in the coming months, supported by solid global demand for semiconductors, electric vehicles, and other green technologies.

Source: Bloomberg, BIL

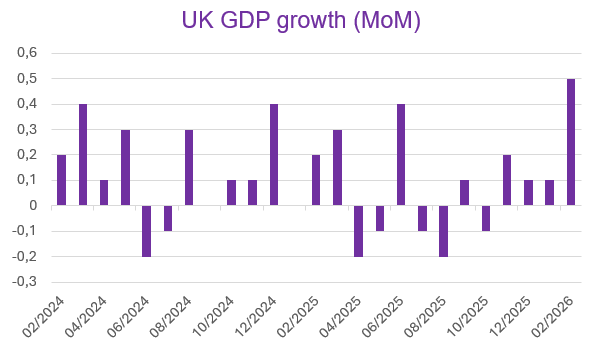

UK economy showed unexpected resilience in February

The UK economy expanded by 0.5% month on month in February, accelerating from January’s 0.1% increase and surpassing expectations. This was the strongest monthly growth since January 2024, driven primarily by a robust performance in the services sector. Both services and production grew by 0.5% in February, while construction output rose by 1%.

Source: Bloomberg, BIL

Although this data predates the escalation of the conflict in the Middle East, it offers some reassurance that the UK economy entered the subsequent energy shock from a stronger position than anticipated. However, as a net energy importer, the UK remains highly exposed to global energy supply disruptions and rising prices. Higher energy costs are therefore expected to push inflation higher over the course of the year, undermining both consumer and business confidence. As a result, the pickup in growth seen in February is unlikely to be sustained.

Earlier last week, the IMF cut its growth forecast for the UK to 0.8% for 2026 and warned that Britain would be negatively affected by higher energy costs. This represented the largest downward revision among G7 countries.

Calendar for the week ahead

Monday – Germany PPI (March).

Tuesday – Japan & Switzerland Balance of Trade (March). UK Unemployment Rate (February), Average Earnings (February). ZEW & Germany Economic Sentiment (April). US Retail Sales (March).

Wednesday – UK Inflation Rate (March). Eurozone Consumer Confidence Flash (April).

Thursday – Eurozone New Car Registrations (March). Eurozone, UK & US Composite, Manufacturing & Services PMI (Flash, April). US Jobless Claims.

Friday – Japan Inflation Rate (March). UK Retail Sales (March). Germany Ifo Business Climate (April). US Michigan Consumer Sentiment (Final, April).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more