BIL INVESTMENT INSIGHTS

Market Snapshot

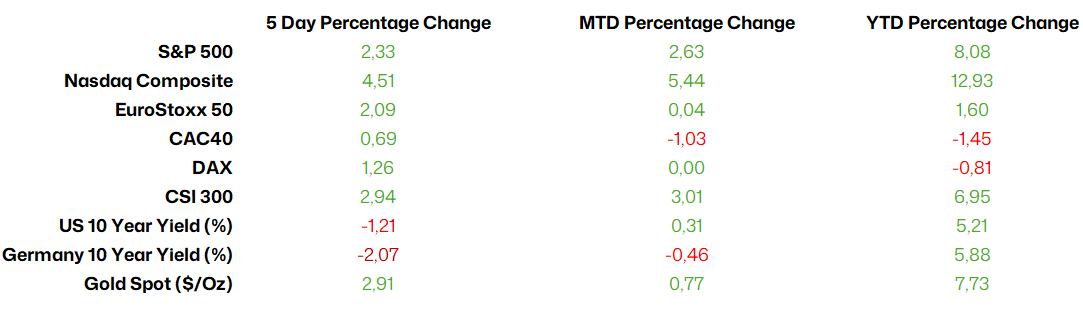

Oil prices rose again over the weekend as Washington and Tehran failed to come to an agreement to end the war in the Middle East. Despite ongoing geopolitical uncertainty, US equity markets rallied last week, driven by strong corporate earnings. Results show broad-based earnings growth, with Technology and Communication Services leading on robust AI and cloud driven demand. Health Care and Energy performance has been more mixed, driven by idiosyncratic factors including drug patent expirations and commodity price volatility. Despite strong overall results, guidance has varied, with greater confidence among companies benefiting from high revenue visibility and more caution among those exposed to geopolitical risks.

In comparison, European earnings results have been more uneven. Although Technology and Industrials have shown relatively more optimistic guidance, earnings growth continues to trail the US, reflecting Europe’s greater exposure to war‑related risks and limited exposure to the AI theme driving the rally in the US.

Source: Bloomberg, BIL as of May 11

Macro Snapshot

ISM PMIs cool as prices heat up

The US ISM Manufacturing PMI remained unchanged at 52.7 in April, matching its highest level since August 2022. 50 is considered the line of demarcation between contraction and expansion. New orders strengthened, rising to 54.1 from 53.5 in March, while supplier delivery times lengthened further (60.6 vs. 58.9). However, production growth eased somewhat (53.4 vs. 55.1), while input prices surged at the fastest pace since late 2021, largely driven by higher oil and diesel costs linked to the Middle East conflict.

The ISM Services PMI fell to 53.6 from 54.0. Business activity showed continued strength, with the output index rising by two points to 55.9, highlighting the resilience of the US economy. Price pressures intensified further, with the prices index climbing to 70.7—its highest level since 2022. Service providers reported higher costs for fuel, gasoline, diesel, copper, and freight, alongside increases in aluminum and lumber prices linked to tariffs. To keep an eye on is the fact that new orders declined sharply, falling by 7.1 points to 53.5.

Overall, employment across the private sector continued to contract.

Source: ISM, Bloomberg, BIL

AI’s Impact on the US Labour Market Becomes Increasingly Evident

Recent data highlight the growing influence of artificial intelligence on the US labour market. Mid-week, the Job Openings and Labor Turnover Survey (JOLTS) reported that job openings declined by 56,000 to 6.866 million in March, slightly above market expectations of 6.84 million. While openings increased in finance and insurance (+98,000), they dropped significantly in professional and business services (-318,000).

The latter is widely considered as one of the sectors most exposed to AI-driven disruption. This adds to a mounting body of evidence pointing to AI’s tangible impact on employment trends. For instance, for a second month in a row, the Challenger layoffs report indicated that roughly one quarter of US job cuts cited AI as a contributing factor.

Source: Bloomberg, BIL

Although history does not repeat itself exactly, it often rhymes. The current shift mirrors past technological transformations: an initial wave of disruption, near-term job losses in vulnerable sectors, followed by offsetting gains that help stabilize overall employment levels. While AI-driven automation may reduce demand for certain white-collar roles, for example, in legal, accounting, and consulting, economic theory suggests a broader, compensating effect. In particular, the Jevons paradox implies that lower production costs can ultimately stimulate greater demand.

Early signs of this dynamic are already visible. Business formation in the US is accelerating, underscoring entrepreneurial responses to new technological opportunities. It is also worth recalling that roughly half of employment growth since 1980 (when the personal computer revolution began) has come from roles that did not previously exist, highlighting the economy’s capacity to adapt and evolve.

Importantly, the adoption of AI is unlikely to follow a linear trajectory. Instead, it will likely unfold unevenly, as organizations navigate strategic priorities, organizational potholes, data readiness, and practical use cases. As a result, labour market adjustments are expected to be gradual rather than abrupt.

In summary, while AI is already reshaping parts of the labour market, it is also poised to create new opportunities, potentially more than offsetting the jobs it displaces today.

US labour market adds 115,000 jobs in April

Looking at actual job creation in the US, it does remain robust for now. Payrolls rose by 115,000 in April, well above economists’ forecasts, and unemployment remained at 4.3%. The data suggests the labour market is holding up despite economic pressure from the war in the Middle East and higher energy costs.

Job gains were concentrated in healthcare, retail, transportation and warehousing, while federal government employment and tech jobs declined. Although hiring slowed from March levels, the energy-price shock has not yet translated into broader job losses.

The resilience of the labour market is also reducing the likelihood of interest rate cuts by the Fed, as solid job growth suggests the broader economy is continuing to hold up. With employment remaining strong, policymakers’ attention has shifted toward assessing how sharply the energy shock will feed into inflation and whether higher fuel costs will keep price pressures elevated.

Markets reacted positively to the report, with US equity futures moving higher.

Eurozone Retail Sales fall for a third month

Eurozone retail sales volumes edged down by 0.1% MoM in March, marking a third consecutive decline. The drop was mainly driven by fuel sales, which fell by 1.6%, their sharpest decrease since August 2023, amid higher fuel prices linked to tensions in the Middle East. Food sales also weakened, declining by 0.3% after a 0.5% fall in the previous month. In contrast, non-food sales provided a bright spot, rising by 0.6% and recording their first increase since November.

Source: Bloomberg, BIL

Calendar for the week ahead

Monday – China Inflation data. US Existing Home Sales.

Tuesday – Japan Household Spending and BoJ Summary of Opinions. Germany Inflation (Final, April). Italy Industrial Production. Germany & Eurozone ZEW Economic Sentiment. US NFIB Small Business Optimism Index. US CPI Inflation (April) and Total Household Debt. China Vehicle Sales.

Wednesday – France Unemployment Rate and Inflation (Final, April). Eurozone GDP Growth (Q1, 2nd Estimate), Industrial Production. US PPI. OPEC Monthly Report.

Thursday – GDP Growth (Q1, Preliminary), Industrial Production and Balance of Trade. Spain Inflation (Final, April). China M2 Money Supply. US Retail Sales, Export & Import Prices, Business Inventories

Friday – Italy Inflation (Final, April). US Industrial Production. Spain Consumer Confidence.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

June 19, 2026

Weekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...

June 16, 2026

BILBoardBILBoard Mid-Year 2026 – In sea...

Sunday, 21 June marks the official start of summer here in the northern hemisphere. Yet, after an unseasonably warm spring, conditions have turned cooler and...

June 15, 2026

Weekly InsightsWeekly Investment Insights

Written as of 15 June, After a volatile week, major US equity indices ended higher on Friday, supported by growing optimism around a potential...

June 5, 2026

Weekly InsightsWeekly Investment Insights

Written as at 5 June 2026 The record-breaking streak among chipmakers paused on Thursday after the outlook from a prominent player cast some doubt...

June 1, 2026

Weekly InsightsWeekly Investment Insights

Written as of 1 June 2026 US stock indices recorded new highs last week with investor optimism around AI serving as the driving force....