BIL INVESTMENT INSIGHTS

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June.

At the first FOMC meeting under Chairman Kevin Warsh, the US Federal Reserve left interest rates unchanged at 3.50%–3.75%, but adopted a more hawkish tone. The dot plot, which captures policymakers’ rate expectations, was revised quite significantly since its last release in March. Three months ago, no committee members expected a rate hike this year and most still anticipated cuts. Now, nine members project at least one hike, while only one still expects easing, indicating that inflation control, rather than employment, has become the Fed’s primary concern within its dual mandate.

Markets were caught off guard. Short-term Treasury yields rose sharply, rate hike expectations were pulled forward to October, and credit spreads widened. Underlying this overhaul, is the inflationary impact of the recent energy shock, which has pushed inflation well above target.

Looking ahead, upcoming inflation data and signals from Chairman Warsh will be critical in shaping expectations, as his policy stance remains a key uncertainty for the US rates outlook. In the meantime, the removal of the Fed’s easing bias has allowed the dollar to regain muscle.

After falling sharply at the beginning of the week, oil prices edged higher on Friday when Iran delayed permanent peace talks, which were scheduled to take place in Geneva, citing renewed Israeli strikes in Lebanon. Iran separately moved to assert control over Hormuz by requiring all vessels to register with the Persian Gulf Strait Authority. At the time of writing, Brent was trading at roughly $79/barrel.

Macro Snapshot

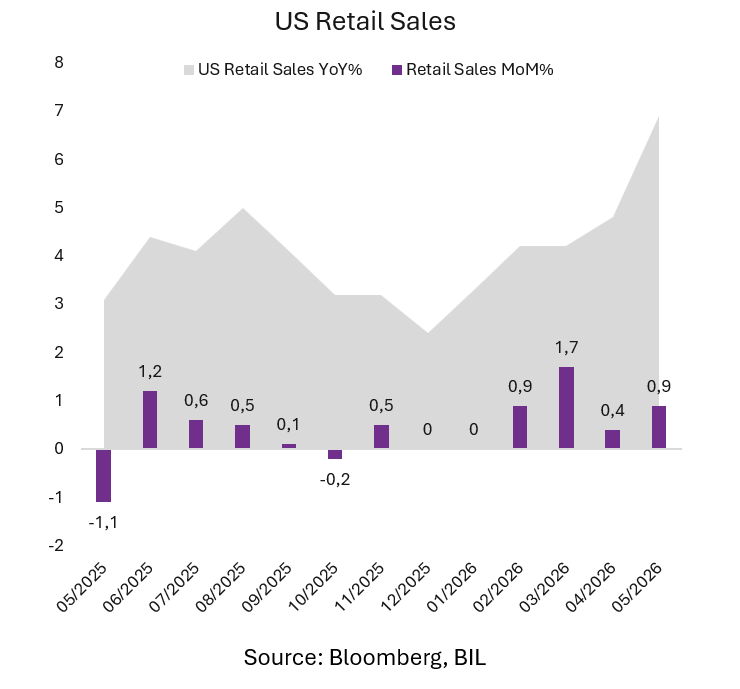

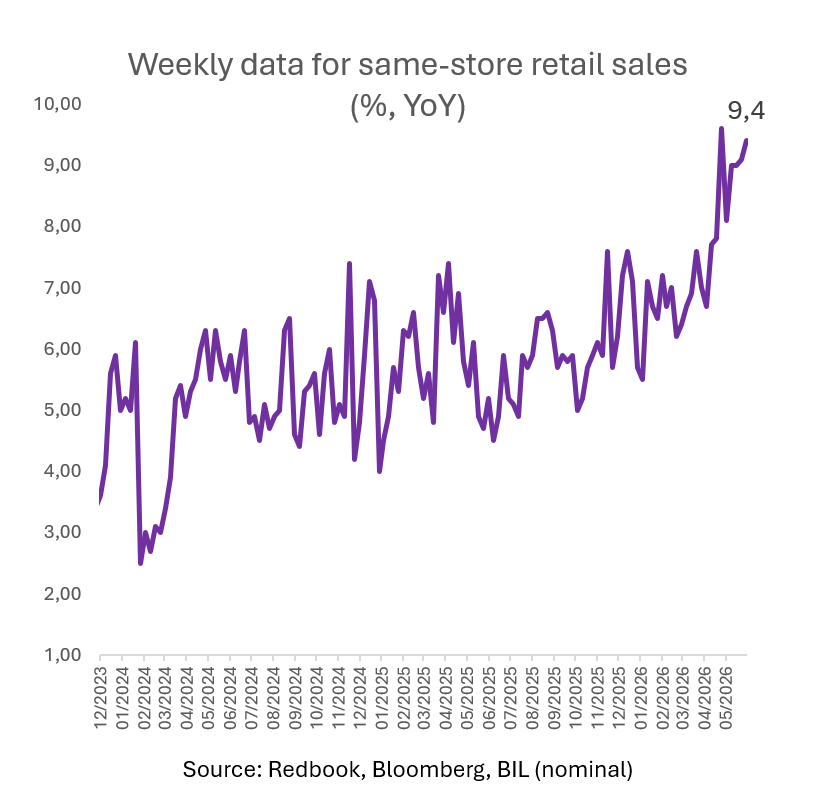

Don’t underestimate the US consumer…

Retail sales in the US increased 0.9% MoM in May, up from 0.4% in April and above forecasts of 0.5%. This latest data release signals that consumer spending has not followed the downward trajectory of consumer confidence.

The data is not adjusted for inflation, so intuitively, gasoline stations accounted for the biggest rise in sales (+3.4% MoM), with prices at the pump pushed up by the ongoing global energy shock.

But even when we exclude this category, core sales, which are used to calculate GDP, were up 0.7%, after a 0.5% gain in April.

The CPI price index rose 0.5% MoM in May.

BoJ lifts rates to highest level since 1995

The Bank of Japan raised its policy rate from 0.75% to 1%, as widely expected, marking its highest level since 1995. The decision was approved by a 7–1 vote, with board member Asada—appointed by Prime Minister Takaichi—dissenting in favour of maintaining the current rate. Governor Ueda did not participate in the vote due to hospitalization. In its statement, the BoJ indicated it will continue to gradually increase the policy rate and adjust the level of monetary accommodation.

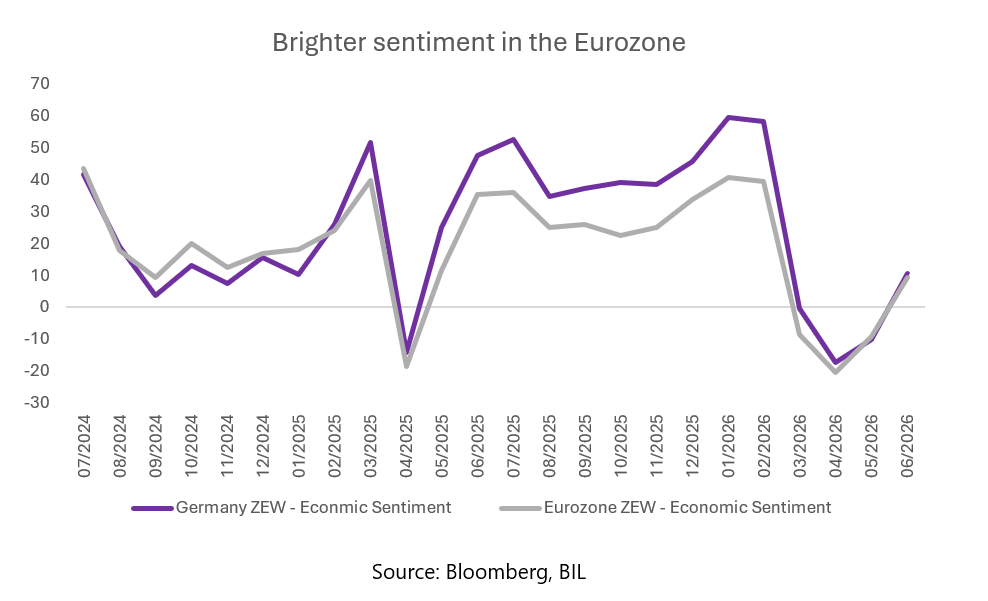

ZEW: Financial analysts become more optimistic on the Eurozone

The latest ZEW Survey - a monthly poll of up to 350 financial analysts and institutional investors – showed improving expectations surrounding both the German economy, and the Eurozone as a whole.

The German Indicator of Economic Sentiment rose 20.7 points to 10.5 in June, trouncing market expectations of -6.0. It marks the first positive reading since the outbreak of war in the Middle East. Improving sentiment was most notable in the auto sector, chemicals & pharmaceuticals, mechanical engineering and private consumption - though all remain sub-zero. The construction saw further declines in its index, falling 15.2 points to -12, most likely as a result of the ECB’s rate hike on June 11.

Zooming out to look at the Eurozone as a whole, the index climbed by 18.6 points to 9.5. Economists had expected a much lower -7.2.

57.7% of analysts expected no change in economic activity, while 25.9% anticipated improvement and 16.4% expected deterioration. The index measuring inflation expectations declined by 19.5 points to 45.8.

UK politics rattle markets as BoE holds rates steady

The dominant story in the UK this week was political: Greater Manchester Mayor Andy Burnham won the Makerfield by-election with 55% of the vote, opening a direct path to challenge PM Keir Starmer for the Labour leadership. Starmer said a contest would send "the country into chaos", but has vowed to stand if there is one. Against that backdrop, the BoE held rates at 3.75% for a fourth consecutive meeting (7-2 vote), with two dissenters pushing for a hike, while May's budget deficit came in at a post-pandemic high of £23.3 billion – up 30% YoY, with much of the surge driven by higher debt interest costs. Gilts sold off on the political risk, with the 10-year yield rising roughly 7 basis points to 4.83%.

Calendar for the week ahead

Monday – Eurozone Consumer Confidence. China Loan Prime Rate.

Tuesday – US, Eurozone, UK, Japan Composite PMI (Flash, June). France Business Confidence.

Wednesday – Germany IFO Business Climate. US Building Permits and New Home Sales. US Fed Bank Stress Test Results.

Thursday – Germany Gfk Consumer Confidence. France Consumer Confidence. US PCE Inflation, GDP Growth (Final, Q1), Personal Income and Spending, Weekly Jobless Claims

Friday – Fed Goolsbee Speech. France Unemployment Data. US Michigan Consumer Sentiment (Final, June)

Saturday – China Industrial Profits

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more