BIL INVESTMENT INSIGHTS

Written 17 July, noon.

Market Snapshot

Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly chipmakers.

In the Middle East, the US continues to strike Iranian infrastructure, while Iran has retaliated by targeting US bases across the region. China and Pakistan have expressed concern and urged both sides to resume dialogue. Traffic through the Strait of Hormuz has all but ground to a halt again, and Brent crude trades above $85/barrel having gained over 10% throughout the week. The Trump administration is keen to restore normal shipping flows through the Strait of Hormuz in order to ease energy market pressures ahead of the US midterm elections. Iran, meanwhile, remains reluctant to relinquish leverage over one of the world's most strategically important waterways.

On the AI front, tech stocks – particularly memory chip makers – suffered from a wave of selling on Friday, as momentum trades were unwound. Traders are increasingly questioning whether the billion-dollar spending spree by hyper-scalers will produce strong enough ROI to sustain elevated chip demand.

On a more positive note, the US earnings season has got off to a strong start. With only around 10% of companies on the S&P 500 having reported, it is too soon to draw overall conclusions. However, thus far, companies are beating elevated expectations and positive guidance momentum has continued. US bulge bracket banks have delivered broadly solid results on exceedingly strong trading activity, and constructive trends in net interest income. Next week, the earnings results of Alphabet, Tesla and IBM will likely garner a lot of attention.

Macro Snapshot

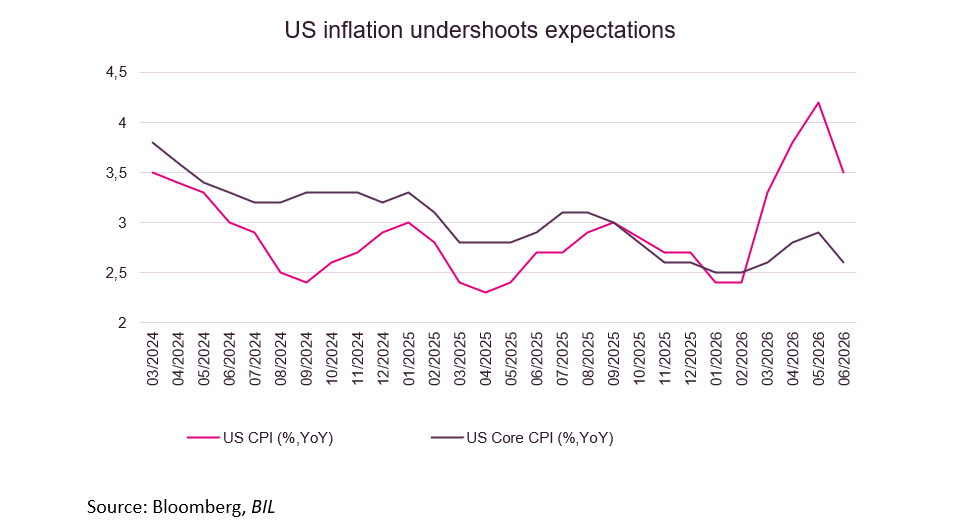

US Inflation falls for the first time since 2020, taking some pressure off the Fed

Consumer prices in the US fell 0.4% MoM in June, well below forecasts of around 0.1% declines. It was the first monthly drop since 2020, bringing the annual inflation rate down to 3.5% (vs. 4.2% in May). Core inflation, which excludes volatile categories such as food and energy, also cooled to 2.6% (vs 2.9%), with the monthly core index unchanged (versus +0.2% expected) – raising hopes that May could prove to have been the peak of this inflation episode. Most of the relief came from energy: with the mid-June ceasefire between the US and Iran calming markets, oil retreated from above $90 to roughly $73 per barrel over the month, and energy costs fell 5.7% - the steepest monthly drop since April 2020 – led by gasoline (-9.7%). Food inflation rose by 0.2% for a second consecutive month, with the annual rate edging down to 3.0%

For the Fed, the details were arguably more important than the headlines. Core goods prices fell for a second month – a tentative sign that the pass-through from trade tariffs may be largely complete. The services gauge, which Fed officials watch closely – fell from 3.4 to 3.2% YoY. The report landed the same day that Fed Chair Kevin Warsh told Congress the central bank has “no tolerance” for persistently elevated inflation and remains committed to restoring price stability. The softer data should allow policy makers to keep that hawkish tone without being compelled to act on it: market-implied odds of a hike at the late-July meeting fell considerably after the release, while September hike odds slipped to around 60% from above 75%. Some economists expect the FOMC to remain on hold at the current 3.5%-3.75% range for the rest of the year – provided renewed hostilities in the Middle East do not reignite energy prices.

Markets welcomed Tuesday's print. Bond yields fell, especially on shorter maturities, the dollar weakened slightly, and US stocks ended the day higher, with technology shares among the main winners as investors trimmed their bets on further rate hikes. Still, one good month does not make a trend. Inflation remains well above the Fed’s 2% goal, price increases are still spread across many categories, and the US-Iran ceasefire has come under renewed strain in recent days.

China's growth slows more than expected, adding pressure for stimulus

China's economy grew 4.3% YoY in the second quarter, below forecasts of 4.5% and a clear step down from 5.0% in Q1. This marked the slowest growth since late 2022, and is below the pace required to comfortably achieve Beijing's full-year growth target of 4.5–5.0%.

The granular details for June point to a two-speed economy. Exports remain the bright spot; they jumped 27%, supported by strong demand for technology products, including chips and other AI-related hardware, while industrial production accelerated to 5.3% (vs. 4.6% expected). At home, however, the picture remains weak: retail sales rose just 1.0% over the month – better than expected, but still far below desired levels.

In further evidence of domestic weakness, fixed-asset investment fell 5.7% in the first half, and the property downturn also deepened, with real estate investment down around 18%. In short, the technology and export sectors continue to support China's manufacturing base, but domestic consumption and real estate remain significant drags on the economy. The disappointing growth figures are likely to increase pressure on policymakers to deliver additional support in the coming months. Investors will therefore closely watch the upcoming Politburo meeting (late July) for signals on the pace and scale of further fiscal and monetary stimulus. Until then, China's growth story is likely to remain heavily reliant on exports and advanced technology sectors, a trend that is causing some frictions with the United States and Europe.

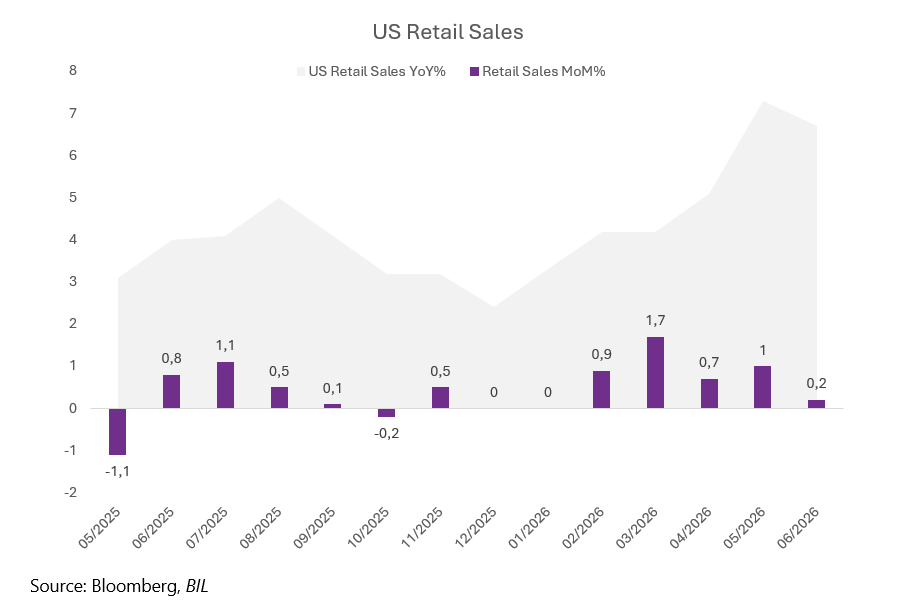

Cheaper gasoline, busy stadiums: US consumers continue spending

American consumers kept spending in June, even if the headline number does not show it at first glance. Retail Sales rose 0.2% over the month, slightly below the 0.3% gain economists had expected, after a strong (upwardly revised) 1.0% increase in May. The weak headline has a simple explanation: Retail sales measure how much money is spent, not how much is bought. Gasoline became much cheaper in June, with pump prices falling by roughly 50 cents per gallon. As a result, spending at gas stations dropped 5.3%, the biggest fall since 2022, pulling the total down. Excluding gas stations, sales rose by a healthy 0.7%, and seven of the thirteen retail categories grew. A core measure that economists use to judge underlying demand also rose 0.5%, exactly as expected.

Part of June’s strength came from special events. Amazon held its Prime Days sale earlier than usual, which lifted online sales by 1.9%, the biggest increase in nearly a year. The FIFA World Cup also boosted spending: according to the Fed's latest Beige Book, visitors filled hotels in host cities such as New York, restaurants and bars sold more on math days, and sporting goods sales rose 1.3%. Beyond these one-off effects, however, underlying demand looks to be intact. Credit card data show spending is rising across all income groups, supported by a stabilising labour market: new jobless claims recently fell to their lowest level since May.

In short, the US economy remains in good shape, which supports the view that the economy can cope with the Federal Reserve’s current focus on fighting inflation. The main near-term risk is a renewed rise in fuel prices: the conflict in the Middle East has flared up once more, and oil prices are climbing again, which could eat into household spending power over the coming months. So far, consumer sentiment is holding up. On Friday, the University of Michigan's Consumer Sentiment Index rose to 54.4 for July, beating expectations of 51.0 and marking a second straight monthly increase.

Tariffs become a topic again with Section 122 coming close to expiry

Last week, the Trump administration announced a new 25% tariff on imports from Brazil, citing concerns over unfair trade practices. However, with inflation still a key concern for voters, and November’s midterm elections fast approaching, several exemptions were made for products that are not produced in sufficient quantities domestically and for which the US relies heavily on Brazilian supply, for example, beef, coffee and orange juice.

The measure is being pursued under Section 301 of the Trade Act, which authorizes the US government to investigate and respond to unfair trade practices by foreign trading partners.

Following the Supreme Court's decision to invalidate parts of the administration's earlier tariff framework, President Trump implemented a temporary universal tariff of 10% under Section 122 of the Trade Act of 1974. The measure is allowed for 150 days and is set to expire on July 24. As that deadline approaches, further tariff announcements are likely, including additional Section 301 actions, as the administration looks for alternative legal mechanisms to maintain or expand import duties.

Calendar for the week ahead

Monday – China Loan Prime Rate, Germany PPI Announcement

Tuesday – UK Employment data, Germany & Eurozone ZEW Economic Sentiment Index.

Wednesday – Japan Balance of Trade, UK Inflation Rate.

Thursday – US Weekly Jobless Claims, ECB Monetary Policy Meeting and Press Conference, Eurozone Consumer Confidence (Flash).

Friday – Japan Inflation Rate, Germany GfK Consumer Confidence, UK Retail Sales. US, Eurozone and UK Composite PMI (Flash, July)

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more