BIL INVESTMENT INSIGHTS

Equities and bonds extended declines last week as investors grew increasingly concerned about the prospect of a prolonged energy shock, following renewed attacks on key energy infrastructure in Qatar and Iran. Iran’s strike on Qatar’s Ras Laffan gas facilities, responsible for roughly 20% of global LNG supply, caused “extensive damage” and pushed global LNG prices sharply higher. Although Gulf LNG exports represent only about 3% of global natural gas consumption, energy markets are priced “at the margin.” This means even a relatively small supply disruption can have an outsized impact on prices. To elaborate, as Gulf LNG volumes fall, major importers such as China, Korea, India, and Pakistan turn to the spot market for replacement cargoes, intensifying competition and driving up LNG and pipeline import prices across Europe and Asia. In short, prices are driven by the small amount of supply or demand that balances the market at the edge, not by the total volume.

As a result of ongoing events, inflation risks have clearly risen. Petrochemicals derived from oil and natural gas are integral to the production of more than 95% of manufactured goods, including plastics, fertilisers, pharmaceuticals, and synthetic fibres. They are also essential inputs for construction, automotive manufacturing, and healthcare. Rising energy costs therefore feed quickly and broadly into the wider economy.

For now, long-term inflation expectations in Europe have moved higher, although not to the extremes seen during the 2022 energy crisis. Expectations in the United States remain more contained. Nevertheless, government bonds on both sides of the Atlantic have come under pressure, reflecting fears that central banks may need to delay or even reverse monetary easing in response to the inflationary impulse from higher energy prices. UK gilt yields have climbed to their highest levels since 2008, supported by recent Bank of England remarks indicating their willingness to raise rates if necessary.

Higher rate expectations weighed on non‑yielding assets, with precious metals experiencing sharp volatility. Gold briefly surrendered its year‑to‑date gains before partially recovering on Monday, while silver fell approximately 10%. Growth concerns also dragged industrial metals lower, and even defensive equity sectors such as consumer staples suffered on fears that rising input costs could erode profit margins. The only sector unscathed was energy.

Over the weekend, geopolitical tensions escalated further. President Trump issued a deadline for Iran to reopen the Strait of Hormuz, threatening strikes on Iranian power plants if it failed to comply. As the deadline approached, Iran continued attacks across the Persian Gulf. Market sentiment improved somewhat on Monday after the US President reported “very good and productive” discussions with Iran regarding a path toward ending the conflict, and postponed potential strikes on Iranian energy assets by five days.

Despite this modest shift in tone, the situation remains highly volatile and unpredictable. It is now clear that hopes for a quick, limited military operation have faded. Even if peace is restored in the coming days, the economic effects of sharply higher energy prices are already feeding through. With critical industrial assets, which were built over decades and at enormous cost, now damaged across the region, the impact on global energy markets will persist long after hostilities cease.

At the start of the year, we expected subdued global growth, with the US better positioned than Europe. The conflict further clouds Europe’s outlook, given its reliance on imported energy. It also effectively removes the prospect of further ECB rate cuts this year and even raises the possibility of a rate increase. The situation is different for the US, a net oil exporter. While US energy availability should remain comparatively secure, higher prices risk reigniting inflationary pressures which were already outside of the Federal Reserve’s comfort zone. Assuming the Fed maintains its independence, the first rate cut now appears more likely to be pushed into 2027 - once the inflationary shock from today’s energy spike has fully dissipated. In the near term, rising gasoline prices pose political challenges for President Trump ahead of midterm elections, increasing pressure on US authorities to mitigate the cost‑of‑living squeeze. Similar relief measures have already been announced in the UK, where households will receive over £50 million to offset rising heating oil costs.

Given the scale of the disruption to global energy markets, we continue to reassess the investment landscape and the assumptions underpinning our asset allocation. We are adjusting our base case as necessary, remaining vigilant and responsive as the situation evolves.

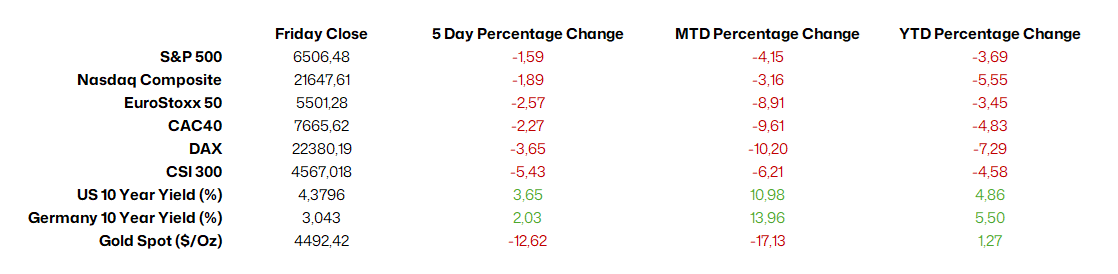

Source: Bloomberg, BIL as of March 23 17:18

Macro Snapshot

Fed holds rates steady and releases fresh economic forecasts

On Wednesday, the US Federal Reserve kept interest rates on hold at 3.5–3.75% for the second consecutive meeting as it waits for more clarity on the impact of the conflict in the Middle East and the resulting surge in energy prices on inflation. Chair Jerome Powell said that, in the short term, “higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy”. The US central bank must tread carefully: inflation was already quite sticky above the 2% target before the situation in the Middle East broke out, while, at the same time, the labour market was cooling rapidly (nonfarm payrolls data unexpectedly reported 92,000 fewer jobs last month).

The Fed also released new economic forecasts showing that officials expect the central bank’s preferred PCE inflation rate to end the year at 2.7%, above the 2.4% forecast in December and well above the 2% target. The Fed's dot-plot still implies one quarter point rate cut this year, in line with the forecasts released in December. However, market expectations for Fed interest rate cuts have decreased sharply on fears of rising inflation, with market participants doubtful that any Fed rate cut will occur, at least not before the second half of 2027. When discussing the forecasts, Powell emphasised that there is still a great deal of uncertainty and that the direction of upcoming monetary policy is undefined.

US stocks fell and the dollar held steady following the announcement. Short-term US government bond yields rose sharply in response to the Fed’s new inflation forecast and surging energy prices.

European central banks keep interest rates steady and warn about inflation

On Thursday, the European Central Bank (ECB) maintained its benchmark interest rate at 2%, as policymakers again awaiting the impact of soaring energy prices on inflation and growth. This decision was in line with expectations, mirroring the actions of other European central banks.

Policymakers expressed concern about the inflationary impact of recent events. Indeed, on Thursday morning, European gas prices surged by 25%, while oil hit $115 a barrel, as strikes on energy infrastructure in the Gulf escalated. Since the start of the conflict, traders have increased their bets on the ECB raising interest rates to combat price pressures instead of keeping rates on hold throughout the year, as had been expected prior to the conflict. The ECB has kept borrowing costs at 2% since June 2025.

Meanwhile, the Bank of England voted unanimously to keep interest rates at 3.75%, stating that the energy shock could start to feed into wages and overall price pressures in the economy. The central bank said that the impact on inflation could become more protracted, requiring tighter monetary policy. This has caused market participants to increase their bets on interest rate hikes by the BoE this year. Prior to the conflict, markets had anticipated that the central bank would cut interest rates at its March meeting, given the decline in inflation and the weakening labour market. Two-year gilts soared on the announcement.

The Swiss National Bank (SNB) kept interest rates at 0% and signalled a greater willingness to intervene in the foreign exchange (FX) market to curb the strength of the Swiss franc. The SNB expects inflation to rise, but is less concerned about it than its European neighbours due to the already lower level of inflation and the strength of the Swiss franc. It raised its near-term inflation forecast to 0.5% year-on-year in Q2 2026 and 0.6% in Q3 2026, but expects the inflationary impact of the conflict to be temporary. However, the central bank warned that there is a lot of uncertainty and that if energy prices rise more strongly than expected, this could push inflation higher and impact growth. Markets are now pricing in a full quarter-point rate hike by the SNB before the end of the year.

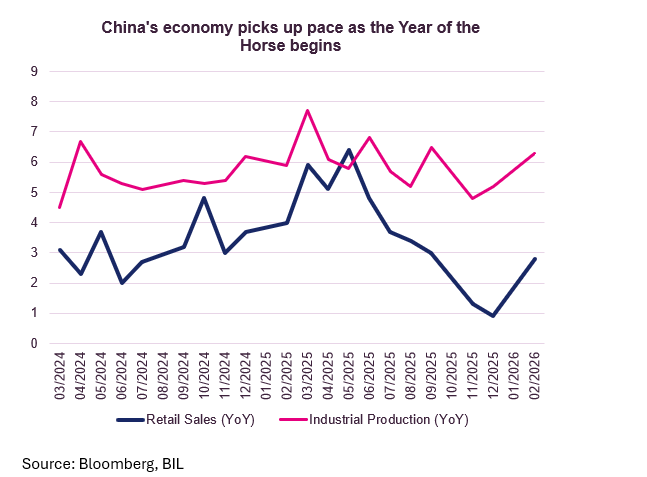

China's economic activity got off to a strong start of the year

China’s industrial production and retail sales increased in January and February, boosting economic activity at the start of the year.

Industrial production rose by 6.3% year on year in the combined January–February period, which is combined to smooth out distortions linked to shifts in the date of the Lunar New Year. This was an acceleration from December's growth of 5.2%, with activity strengthening across major sectors including mining, manufacturing, and utilities.

Fixed asset investment increased by 1.8%, following a 3.8% fall in 2025. Infrastructure investment grew by 11.4% and manufacturing investment increased by 3.1%, more than offsetting the 11.1% decline in property investment.

This pick-up in activity was likely externally-driven, given that exports surged by 21.8% during the same period.

Retail sales increased by 2.8%, accelerating from a 0.9% rise in December. This exceeded expectations and marked the strongest growth since October last year. The extended Lunar New Year holiday boosted consumer spending across the country, with spending increasing on a range of goods and services. Sales of grains, oil and food products, as well as clothing, footwear and textiles, increased sharply. Hotel reservations and duty-free purchases also increased. However, sales declined for petroleum and related products, as well as automobiles.

However, the National Bureau of Statistics noted that geopolitical risks have continued to rise since the period covered by the report, which could present challenges for companies in the months ahead.

This month, China announced a GDP growth target of between 4.5% and 5% for this year, which is below the target of around 5% for 2025, as Beijing faces the challenge to boost consumption as a contributor to GDP growth, as its traditional growth engine of manufacturing and exports faces increasing external threats.

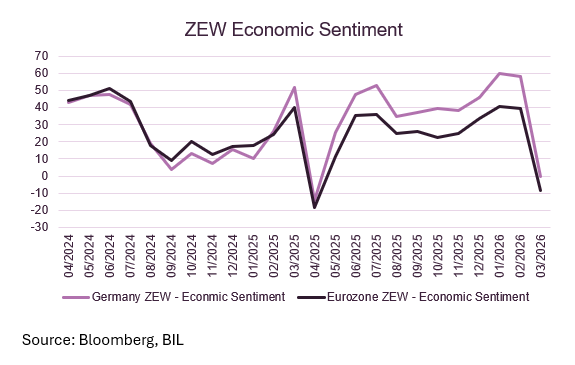

Euro Area Sentiment Plummets Amid Geopolitical Strains

The latest ZEW Indicator of Economic Sentiment for the Euro Area recorded an unexpectedly sharp downturn in March, falling by 47.9 points from the previous month to –8.5 — its lowest reading in 11 months and far below market expectations of 24. This sudden drop highlights deepening concern among financial analysts as geopolitical tensions continue to weigh on the economic outlook.

Germany — typically regarded as the bellwether for European economic momentum — registered an even more dramatic shift. The German ZEW indicator plunged by 58.8 points to –0.5, a stark contrast to market expectations of 39.

The path forward remains clouded, and the extent of economic impact will hinge heavily on the conflict’s duration and severity. For now, sentiment remains sombre with respondents clearly doubtful that a swift resolution is likely, suggesting that uncertainty may continue to overshadow European economic prospects in the months ahead.

Calendar for the week ahead

Monday – Eurozone Consumer Confidence (Flash, March).

Tuesday – Japan Inflation Rate (February). EU New Car Registrations (February). Eurozone, UK, US Manufacturing, Services & Composite PMIs (Flash, March).

Wednesday – UK Inflation (February). Germany Ifo (March). Switzerland Economic Sentiment (March).

Thursday – Germany Consumer Confidence (April). US Jobless Claims.

Friday – UK Consumer Confidence (March), Retail Sales (February). US Michigan Consumer Sentiment (Final, March).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more