BIL INVESTMENT INSIGHTS

Kindly note that our Weekly Insights will pause over the upcoming bank holiday weekend.

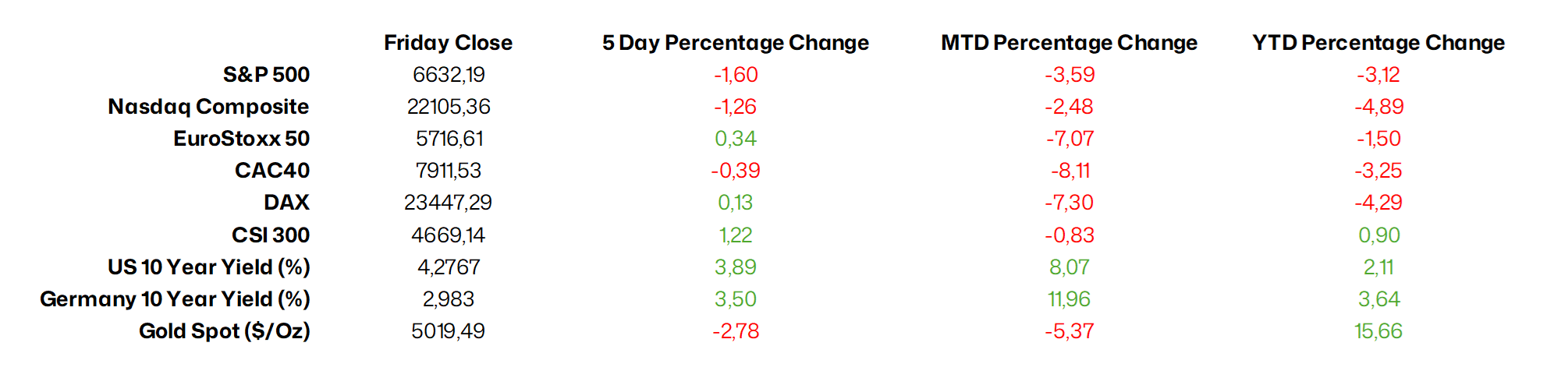

Market Snapshot

The conflict in the Middle East has now extended into its fifth week, and geopolitical headlines continue to dominate market sentiment. In the month since the conflict began, stocks and bonds have suffered their biggest combined sell-off since 2022 as the surge in oil prices raises the prospect of a more persistent inflation shock, prompting investors to reassess expectations for monetary policy. Gold, despite its traditional safe‑haven reputation, has also seen notable volatility since the conflict began. After reaching a record high of $5 400 per ounce in January, the yellow metal has fallen to a level of around $4 600 per ounce. The reason for this is twofold. Firstly, gold has been the victim of profit taking, as investors rush to crystalise gains as other asset classes struggle. Secondly, rising Treasury yields, which reduce the appeal of non-yielding bullion, has led investors to look for shelter elsewhere.

Last week, US stocks experienced their worst day since the conflict began as President Trump failed to reassure investors that an end to the conflict was in sight when he extended his deadline to reach an agreement with Iran. Stocks extended their decline on Monday and Brent crude rose to $116 a barrel as the conflict escalated over the weekend with strikes on aluminum plants in Abu Dhabi and Bahrain and President Trump saying that the US could “take the oil in Iran”. European and Asian stocks also fell.

Source: Bloomberg, BIL as of March 30

Macro Snapshot

OECD warns of the inflationary impact of the conflict in the Middle East

In a new forecast, the OECD warns that the conflict in the Middle East is poised to push US inflation sharply higher, lifting it to 4.2% this year. Elevated energy costs driven by the conflict in the Middle East are expected to ripple through global markets, intensifying price pressures in countries ranging from China to India. The organisation cautions that an extended period of expensive oil and gas would feed directly into production costs and consumer prices, undermining growth.

According to the OECD, this shock has erased the tentative upgrades to global growth forecasts seen at the start of the year, with higher energy prices, disrupted trade routes and pressure on critical commodities such as fertiliser and industrial gases compounding the strain. The US economy is expected to slow as household spending cools, though the Federal Reserve is still projected to keep rates steady. Meanwhile, global inflation projections have been revised upward, and Eurozone growth is set to remain subdued. The organization is now forecasting Eurozone growth of 0.8% for the year, down from its previous estimate of 1.2%. The OECD emphasises that if energy markets tighten further, global output could fall short of baseline forecasts and inflation could rise even more.

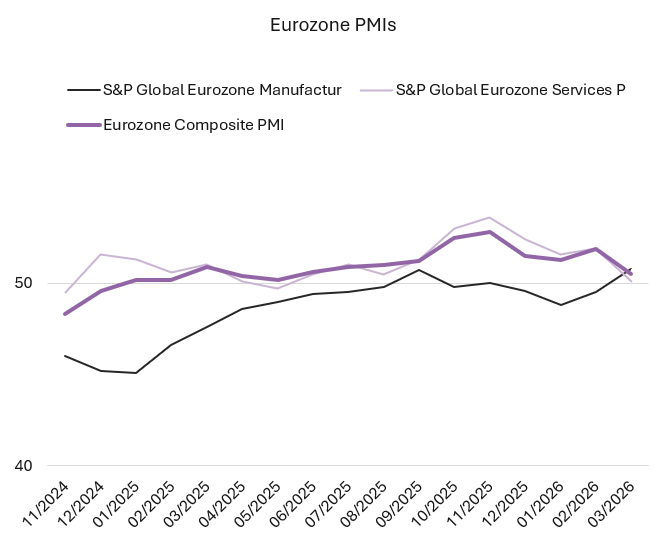

Eurozone business activity weakens to a ten-month low

Business activity around the world has been hit by the conflict in the Middle East and flash estimates last week showed that the Eurozone is no exception The composite PMI fell to 50.5 in March, just above the 50 threshold that separates growth from contraction, indicating only marginal growth in the bloc’s private sector. New orders contracted for the first time in eight months and employment continued to fall amid rising uncertainty related to the ongoing conflict. Price pressures increased, with input cost inflation surging to its fastest pace since February 2023 and output prices rising at the fastest pace since February 2024.

Manufacturing activity increased slightly to 51.4 from 50.8 in February, with new orders rising and export activity showing signs of stabilising. However, manufacturers reported a significant increase in supplier delivery times, reflecting supply chain disruptions linked to the conflict in the Middle East. Services activity fell to 50.1 in March from 51.9 as new orders continued to decline.

Business sentiment fell to its lowest level in ten months, with companies growing increasingly concerned about the fallout from the conflict in the Middle East.

Source: Bloomberg, BIL

UK inflation held steady at 3% in February

In February, consumer prices in the UK grew by 3%, the same as in January and in line with expectations. Prices rose for clothing, housing and utilities, while increases slowed for transport, food, recreation and culture, and restaurants and hotels. Services inflation, which the Bank of England (BoE) closely monitors to gauge price pressures, slowed from 4.4% to 4.3%. Conversely, core inflation, which excludes volatile categories such as food and energy, increased slightly from 3.1% to 3.2%.

Prior to the conflict in the Middle East sparking fears of an energy shock, the BoE had expected the inflation rate to ease to its 2% target by Q2 of this year. However, since the conflict began, there have been growing expectations that the energy supply shock will start to affect price pressures around the world, including in the UK. Last week, the central bank held interest rates steady and expressed its readiness to raise them to keep inflation in check. Prior to the conflict, market participants had expected the BoE to cut interest rates in March as inflation eased. Instead, market pricing now suggests two quarter-point rate rises this year.

UK retail sales fall as consumers rein in spending

After the strongest growth in a year and a half in January, British retail sales fell by 0.4% month-on-month in February, as sales at supermarkets and household goods stores fell, with retailers citing bad weather as dampening demand. Online retailers also experienced a modest slowdown, as many consumers had already shifted their spending into January to capitalize on post‑holiday promotions.

Earlier on Friday, the GfK consumer sentiment survey showed that morale had fallen to its lowest since April 2025, as the conflict in the Middle East has clouded the outlook for inflation and thus, consumers future spending power.

These data releases add to already mounting economic headwinds, as business activity softened in March and ongoing geopolitical tensions have put the Bank of England in a waiting mode while it assesses the inflationary impact of the conflict.

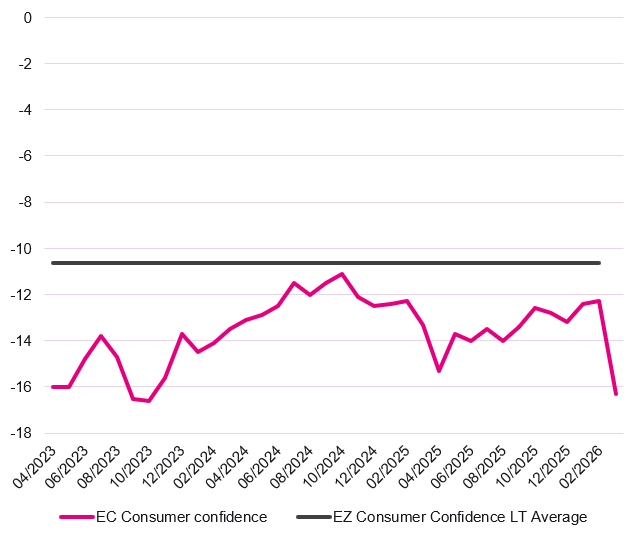

Consumer confidence falls sharply across the EU

Consumer confidence in the Eurozone decline by 4 points to -16.3 in March, the lowest since October 2023, and worse than forecasts of -14.4. The drop was driven primarily by the conflict in the Middle East and the resulting impact on energy prices and inflation. In the broader European Union, consumer sentiment plummeted by 3.4 points to -15.2. With both indicators now at their lowest levels since October 2023, well beneath their historical averages, the data suggests that European consumers are bracing for a more challenging economic trajectory in the months ahead.

Source: Bloomberg, BIL

Calendar for the week ahead

Monday – Switzerland KOF Leading Indicators (March). Eurozone Economic Sentiment (March), Consumer Confidence (Final, March).

Tuesday – Japan Unemployment Rate (February). China NBS Manufacturing & Non-Manufacturing PMI (March). UK GDP Growth Rate (Final, Q4). Eurozone Inflation Rate (Flash, March). US JOLTS Job Openings & Quits (February), CB Consumer Confidence (March).

Wednesday – Switzerland Retail Sales (February), Manufacturing PMI (March). Eurozone, UK & US Manufacturing PMI (Final, March). Eurozone Unemployment Rate (February). US Retail Sales (February), ISM Manufacturing PMI (March).

Thursday – Switzerland Inflation Rate (March). US Challenger Job Cuts (March), Balance of Trade (February), Jobless Claims.

Friday – US Non-Farm Payrolls (March), Unemployment Rate (March) Services & Composite PMI (Final, March), ISM Services PMI (March).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more