BIL INVESTMENT INSIGHTS

Central bank communication was a key market driver last week, with several officials taking the mic.

Stateside, Richmond Fed President Tom Barkin warned that US inflation remains "too high" and reiterated his support for a moderately restrictive monetary policy stance. Speaking at the Aspen Ideas Festival, he acknowledged that easing oil prices following the Middle East ceasefire could provide some relief, but highlighted that AI-related infrastructure investment, resilient consumer spending and corporate pricing behaviour could all lead to more embedded inflation.

Attention then shifted to the ECB Forum in Sintra. In her speech, Back to Basics in an Uncertain Environment, ECB President Christine Lagarde argued that the euro area's improved resilience means the ECB no longer needs to rely heavily on unconventional policy tools such as large-scale asset purchases, emergency lending programmes or detailed forward guidance. Instead, policymakers can employ policy rates as their primary instrument for maintaining price stability. Lagarde stressed that decisions will remain data-dependent and taken meeting by meeting, adding that "forward guidance is not in the cards."

Other ECB officials broadly reinforced the message that policy will remain data dependent. While opinions differ regarding the need for further tightening, the Governing Council appears firmly in a holding pattern, awaiting additional evidence on inflation and economic activity before signalling its next move.

US Fed Chair Kevin Warsh echoed Lagarde's reluctance to provide forward guidance. Speaking in Sintra, he declined to indicate what the Fed might do at its upcoming meeting, while emphasising that inflation remains above acceptable levels and reaffirming the Fed's commitment to restoring price stability. Overall, his message pushed back against suggestions that he would pursue a more dovish policy stance simply because he was appointed by President Trump.

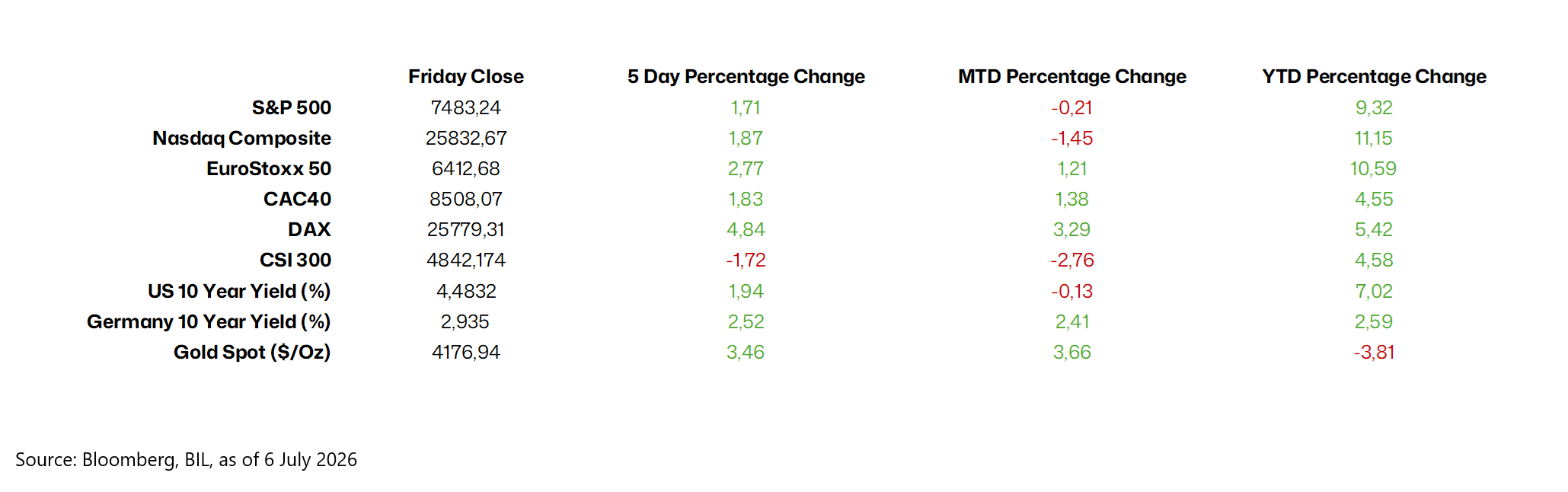

In equity markets, Europe's benchmark indices reached new record highs as investor sentiment improved on the back of lower oil prices, easing concerns about a prolonged energy supply shock and softer-than-expected inflation readings.

In the United States, however, some steam was released from the AI rally, with semiconductor stocks in particular facing profit-taking. Market leadership broadened as investors rotated into overlooked sectors. This was perceived as a healthy market rotation rather than a broad risk-off move, with capital shifting from richly valued mega-cap technology stocks towards cyclical and value-oriented sectors. That said, by Monday, at the time of publication, tech stocks were already bouncing back.

Macro Snapshot

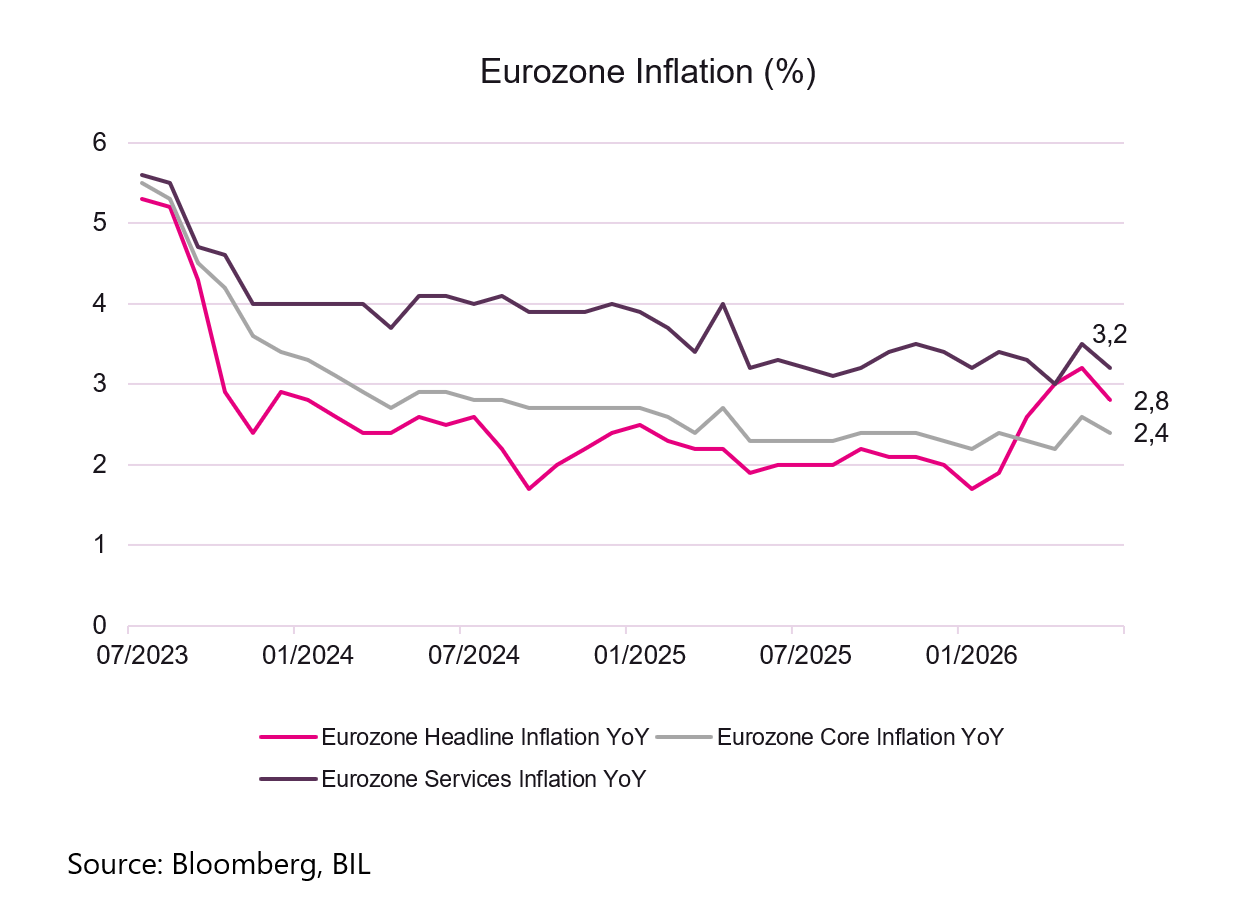

Price pressures in the Eurozone ease more than expected

Consumer price inflation in the Euro Area fell to 2.8% in June, down from 3.2% in May and below market expectations of 3.0%, according to flash estimates. This represents the lowest inflation reading since February, prior to the outbreak of the conflict in the Middle East, which disrupted global energy markets. Albeit, inflation remains above the ECB's 2.0% target, for a fourth consecutive month.

The moderation was supported by lower energy prices, with Brent crude falling 26% during June to around $72 per barrel, leading energy inflation to ease to 8.7% from 10.8%. Inflation also slowed in services (3.2% vs. 3.5%) and food, alcohol and tobacco (1.6% vs. 1.9%), while non-energy industrial goods inflation remained unchanged at 0.9%.

Core inflation, which excludes the more volatile energy and food components, declined to 2.4% from 2.6%, indicating that underlying price pressures are gradually easing. Across the major Eurozone economies, inflation slowed in Germany (2.4% from 2.7%), France (2.0% from 2.8%) and Italy (3.1% from 3.2%), while remaining constant in Spain at 3.6%.

In Luxembourg, the harmonised inflation rate fell further to 3.8% in June, according to Eurostat, but it remains among the highest in the Eurozone. Statec has yet to publish its June inflation estimate, which may differ from the Eurostat figure owing to methodological differences.

Germany Unveils Broad Reform Package to Support Growth

Germany's coalition government unveiled its "Programme for Growth and Employment", a broad reform package aimed at boosting competitiveness, investment and long-term growth. Key measures include EUR 10 billion per year in income tax relief for low- and middle-income households from 2027, a gradual reduction in corporate taxation, labour market reforms, significant deregulation efforts and a structural pension overhaul linking retirement age to life expectancy after 2031. While economists and business groups broadly view the package as one of Germany's most ambitious reform efforts in years and expect positive medium-term growth effects, most stop short of calling it transformational. Importantly, none of the measures have been enacted yet: several require separate legislation, Bundesrat approval and effective implementation by Germany's federal states and local authorities, particularly regarding the planned reduction of bureaucracy and faster permitting procedures.

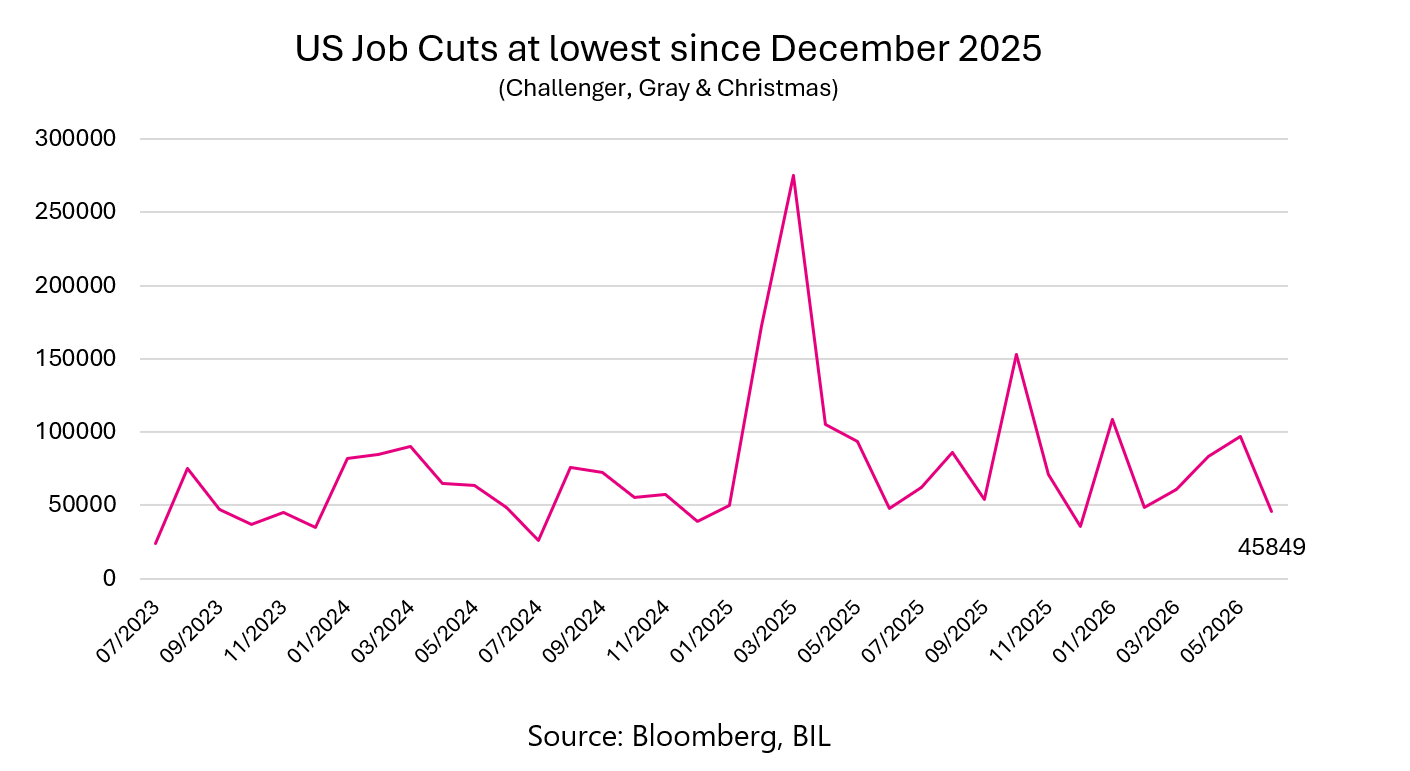

US employers aren’t firing, but remain cautious on hiring

Last week, we had a slate of data allowing us to take the pulse of the US labour market. First, the Challenger report revealed that the pace of layoffs decelerated in June. Job cuts are down 53% from May and hover 4% lower than in the same month in 2025. Where layoffs did occur, they were largely concentrated in the tech sector (15,503), with AI leading companies to re-think their staffing needs.

Then, the JOLTs survey (job openings and labour turnover), sent another encouraging signal: job postings are on the rise. The number of vacancies rose by 9000 to 7.6 million, the highest level in two years, and comfortably above market expectations of 7.3 million.

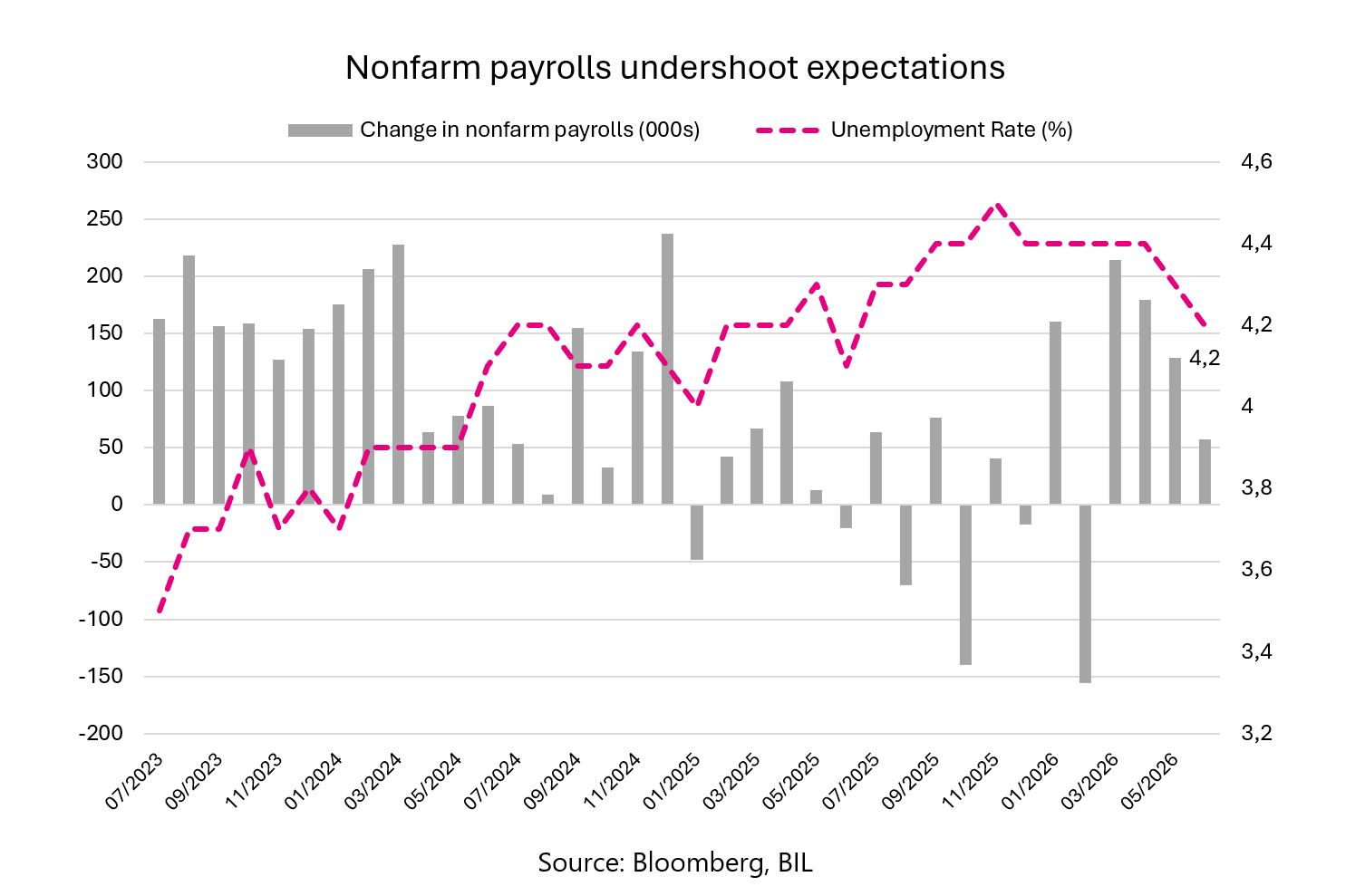

However, stronger labour demand has yet to translate into a meaningful pickup in hiring. Nonfarm payrolls increased by just 57,000 in June, well below expectations of around 110,000, indicating that many employers remain cautious about expanding headcount. Gains were concentrated in business and professional services (a sign that AI cannot yet fully replace people), healthcare and social assistance.

The unemployment rate edged down to 4.2% from 4.3%, largely reflecting a sharp decline in labour force participation. The participation rate fell to 61.5% from 61.8%, while the labor force contracted by 720,000 people.

Calendar for the week ahead

Monday – Germany Factory Orders. Eurozone PPI and Retail Sales. US ISM Services PMI. US S&P Composite PMI (Final, June).

Tuesday – France Balance of Trade. UK House Price Index and BoE Financial Stability Report.

Wednesday – US FOMC Meeting Minutes.

Thursday – China Inflation data (June). US Weekly Jobless Claims, Speech by the Fed’s Williams, Existing Home Sales.

Friday – Germany, France HICP Inflation (Final, June). Italy Industrial Production.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more