BIL INVESTMENT INSIGHTS

Echoing the old adage that innovation is often overestimated in the short-term but under-estimated in the long run, US tech stocks lost momentum this week amid concerns of an emerging AI bubble. A recent MIT study found that only 5% of companies are currently generating returns on their AI investments. This weighed quite heavily on the tech-focused NASDAQ composite, despite a run of strong earnings. After such a rapid valuation surge, some volatility might have been expected, and highlights that AI should be viewed as a long-term structural theme within portfolios. Selectivity will be critical, as investors seek to identify the true beneficiaries of a growing set of monetization opportunities, while avoiding those that will be left behind.

Towards the end of the week, US stocks halted their slide while those in Europe hovered near all-time highs, as all eyes turned to Fed’s Annual Economic Policy Symposium in Jackson Hole, where Jerome Powell delivered his long-awaited speech on the outlook on monetary policy. Following his speech, US government debt and US stocks rallied.

More details of the US-Europe trade deal were outlined in a joint statement released by Washington and Brussels on Thursday, confirming the 15% cap on US tariffs on key EU goods exports including pharmaceutical goods, lumber and semiconductors. However, these sectors are not entirely safe from higher duties, as they remain subject to ongoing US national security investigations that could result in increased tariffs. From September, the US will also reduce tariffs on unavailable natural resources (including cork), all aircraft and aircraft parts, generic pharmaceuticals and their ingredients, and chemical precursors to pre-January levels.

In return, the EU has promised to purchase significant quantities of energy and AI technology from the US, grant preferential market access for a range of seafood and agricultural products, and reduce tariffs on all US industrial goods to zero. To the detriment of Germany in particular, the US will maintain a 27.5% tariff on EU cars until the lower tariffs on US goods are set in stone: this could take some time as it requires the approval of the member states and possibly the European Parliament.

Weekly Highlights

Powell opens the door for a September rate cut

Policymakers from around the world gathered in Jackson Hole Wyoming this week for the annual Kansas City Fed Economic Policy Symposium. The burning question is: Will the Fed cut rates next month? Powell seemed to pave the way for this.

Given that the last monetary policy meeting revealed a divided group of rate setters, it was unsure whether the Fed would be able to give a clear direction of monetary policy.

Clearly, data showing significant weakening in the labour market has caught the Fed’s attention. Powell struck a dovish tone, stating, “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance”. The statement gave markets participants enough confidence that an interest rate cut is on the way – and now, futures markets are almost fully pricing in a 25 basis point cut in September, with a second one expected by year end. Powell also noted that the impact of the trade war is now visible on consumer prices, and signaled that the impact would likely be a one-off shock rather than long-lasting.

We identify three key reasons why this might be the case:

- Businesses are unlikely to pass on the full cost of tariffs to consumers, instead absorbing some of the cost themselves and putting pressure on their suppliers to do the same.

- Moderating job growth and softening consumer sentiment make price increases more difficult.

- Businesses are nimble and will likely reconfigure supply chains over time to avoid some of the tariff impact.

The speech might be considered a win for President Trump, that has repeatedly called for the Fed to cut interest rates this year to support the economy.

US

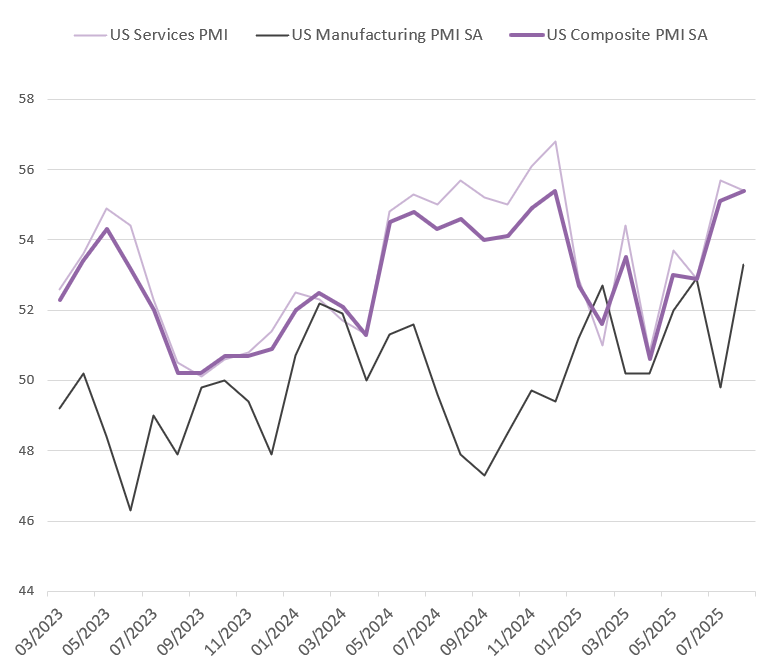

Fears about a slowing labour market (weekly jobless claims overshot expectations) were somewhat alleviated by a solid set of PMIs. According to preliminary estimates, US private sector activity grew at the fastest pace this year with the composite PMI coming in at 55.4. Solid growth was seen in both services and manufacturing with both PMIs well-above the growth threshold of 50. The manufacturing PMI increased to a 39-month high of 53.3, boosted by a large increase in new orders.

Both sectors noted an uptick in hiring, however, input costs continued to rise sharply, mainly due to tariffs, fuelling the steepest increase in average selling price seen in the past three years.

Source: Bloomberg, BIL

With the composite measure PMI at 55.4, US business activity grew at the fastest pace this year and suggests strong Q3 growth (S&P global sees it consistent with 2.5% annualized growth, slightly above the 2.3% implied by the Atlanta Fed’s GDPNow tracker).

The S&P Global report on the PMI concluded that “combined with the upturn in business activity and hiring, the rise in prices signaled by the survey puts the PMI data more into rate hiking, rather than cutting, territory according to the historical relationship between these economic indicators and FOMC policy changes”.

Europe

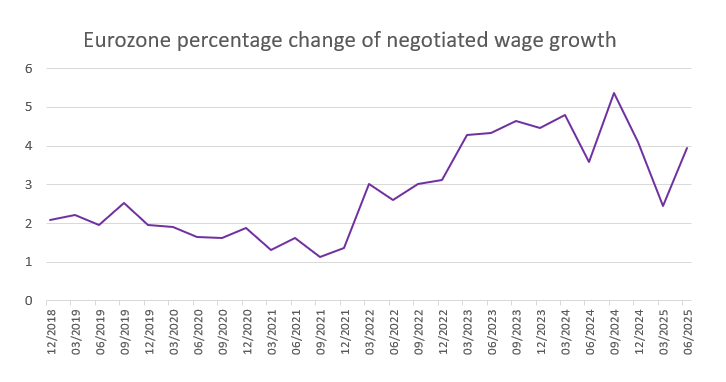

A surprising development in the Eurozone this week, was Friday’s data showing that negotiated wage growth in the bloc rose 3.95% YoY in Q2, from an upwardly revised 2.46% in the previous quarter. The ECB pays close attention to this data point and has emphasised that sustaining its 2% inflation target depends on slower pay gains and cooling price pressures in services, where inflation remains stuck near 3%. The uptick can somewhat be explained by a strong uptick in German wages during the quarter, and the Bundesbank expects this to fade out as inflation eases and the economy stays weak. The ECB’s own pay tracker points to softer wage growth across the bloc into next year.

Source: Bloomberg, BIL

Despite an unexpected rise in wages, Eurozone consumers were not feeling more upbeat. Consumer confidence decreased to -15.50 points in August, from -14.70 prior.

Corporates, on the other hand, are showing improved sentiment following the announcement of the trade deal with the US. According to preliminary PMI data, Eurozone businesses saw new orders increase for the first time since May 2024 in August, helping the composite PMI rise to 51.1. Economic activity has picked up in both manufacturing and services, with the manufacturing PMI rising above the growth threshold to 50.5 for the first time in over three years. Activity in the services sector continued to expand, albeit at a slower pace of 50.7, easing slightly from July’s 51. Germany recorded its fastest growth since March, driven by a strong manufacturing expansion. In France, the downturn eased to the smallest decline in a year.

The unexpected increase in activity, combined with higher inflation pressures in the services sector, bolsters the case for a pause in ECB easing – at least until the effect of tariffs becomes more visible through autumn. Markets currently expect one more 25bp cut this year, but not until December.

Price pressures continued to rise in the United Kingdom in July. The annual inflation rate increased to 3.8%, the highest level since early 2024, up from 3.6% in June and exceeding market expectations. This increase was largely driven by a surge in airfares, likely reflecting the timing of the summer school holidays. Services inflation, which the Bank of England (BoE) closely monitors when setting rates, also rose from 4.7% in June to 5%. As the BoE was strongly divided when deciding to cut interest rates earlier this month, this stubborn inflation suggests that the central bank may slow its already gradual pace of monetary easing.

In Switzerland, companies are still estimating the impact of the 39% tariff imposed by President Trump earlier this month. Many companies that export large quantities of products to the US will find it difficult to pass on the full cost increase to their customers and will need to find more than one way to absorb the cost of tariffs. Some companies have already built up stocks in the US in anticipation of higher tariffs, which gives them more time to plan their next steps. It could therefore take several months before the tariff costs start to impact these companies' margins. In July, exports to the US rose by only 1.1%, slowing from June’s 25.2% surge to frontload potential higher tariffs.

The uncertainty surrounding US trade policy has already impacted the economy. Industrial production in Switzerland contracted by 0.1% YoY in Q2, following strong growth of 8.9% in Q1. This was the first decline in industrial activity since the beginning of 2024 and was driven by lower output in energy supply and construction. Additionally, manufacturing growth slowed to significantly to 0.7%.

Calendar for the week ahead

Monday – Germany Ifo Business Climate (August).

Tuesday – France Consumer Confidence (August). US Conference Board Consumer Confidence (August).

Wednesday – Germany GfK Consumer Confidence (September). Switzerland Economic Sentiment Index (August).

Thursday – EU New Car Registrations (July). Switzerland GDP Growth Rate (Q2). Eurozone Economic Sentiment (August), Consumer Confidence (Final, August). US GDP Growth Rate (2nd Est, Q2), Jobless Claims.

Friday – Japan Unemployment Rate (July), Industrial Production (Prel, July), Retail Sales (July), Consumer Confidence (August). Germany Retail Sales (July). France, Germany, Italy & Spain Inflation Rate (Prel, August). Switzerland KOF Leading Indicators (August). US Goods Trade Balance (Adv, July), PCE Price Index (July), Michigan Consumer Sentiment (Final, August).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

March 2, 2026

Weekly Investment Insights

Market Snapshot Global stocks fell and oil and gas prices spiked on Monday as tensions in the Middle East escalated. On Saturday, the US and...

February 23, 2026

Weekly InsightsWeekly Investment Insights

The US Supreme Court has ruled that President Trump’s trade tariffs are illegal. In a decision issued on Friday, the court found that Trump had...

February 16, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Major US stock indices ended last week in the red, as concerns that AI could have a disruptive impact on entire industries continued...

February 9, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Japanese stocks soared to record levels on Monday as Prime Minister Sanae Takaichi secured a landslide win in a snap general election. The...