BIL INVESTMENT INSIGHTS

Market Snapshot

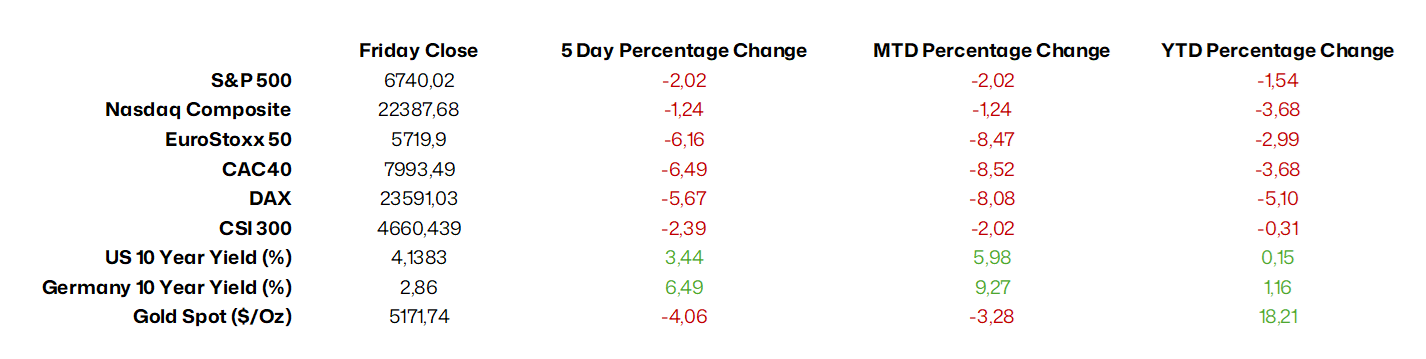

Global markets fell sharply on Friday as Middle East tensions escalated. With traffic through the Strait of Hormuz largely halted, Qatar’s state‑run energy company suspended LNG production following Iranian attacks, pushing Brent crude above $91 per barrel. Over the weekend, additional supply cuts from major producers sent crude briefly surging to $119.50, before easing back toward $105 after news that G7 finance ministers were considering a coordinated release from strategic reserves. Meanwhile, Iran named the son of the late Ayatollah Ali Khamenei as its new supreme leader, with the Islamic Revolutionary Guard Corps pledging allegiance. Major importers of crude—including South Korea, China, Japan, India, Germany and Italy—remain particularly exposed to price shocks, a vulnerability reflected in the steep declines seen across their national equity indices. By contrast, the United States, now a net exporter of oil, has so far experienced more contained market losses.

Fixed income markets also came under pressure as investors revised their inflation expectations higher following the sharp rise in energy prices. A clear divergence emerged between regions: in the United States, inflation expectations remained relatively contained, while in Europe they moved noticeably higher. For now, markets are focused squarely on inflation rather than the potential drag on growth from ongoing energy disruptions, something which is reflected in stable credit spreads. Should attention shift toward growth risks, however, there is a meaningful possibility of spread widening and yield curves moving lower. At our most recent asset allocation committee, we further reduced duration and held the proceeds in cash.

Source: Bloomberg, BIL as of 9 March 2026

Macro Snapshot

Eurozone price pressures edge up while geopolitics rekindle inflation fears

Annual inflation in the Euro Area rose from 1.7% to 1.9% in February, exceeding market expectations for stability. Price pressures were notably stronger in services, where inflation rose to 3.4% from 3.2%, and in non‑energy industrial goods, which climbed to 0.7% from 0.4%. Energy prices continued to fall but at a slower pace, declining 3.2% after a 4.0% drop in January. Inflation for food, alcohol and tobacco remained steady at 2.6%.

Core inflation, which excludes volatile categories like energy, food, alcohol and tobacco, picked up to 2.4%, rebounding from January’s four‑year low of 2.2%. Among the largest Euro Area economies, the Harmonised Index of Consumer Prices (HICP) rose in France (1.1% vs. 0.4%), Spain (2.5% vs. 2.4%) and Italy (1.6% vs. 1.0%), while easing slightly in Germany (2.0% vs. 2.1%).

On a monthly basis, Eurozone headline inflation rose by 0.7%, marking the strongest increase since March 2024.

Renewed inflation concerns have emerged following the escalation of conflict in the Middle East. Higher oil and gas prices, supply chain disruptions and a weaker euro—driven by a flight to safety that boosted the US dollar—are all contributing factors. Because gas stations pass costs on to drivers in a matter of days, the price impact could show quite quickly in the data if the conflict continues to limit energy production or shipments beyond a few days.

Inflation had been forecast to remain below the ECB’s 2% target in both 2026 and 2027.

Following the outbreak of the conflict, interest rate swap markets increased the probability of a rate hike by the ECB in 2026 to almost 50%. We keep our call for unchanged ECB rates this year. For the ECB, the shock could create a difficult trade-off. In the near term, higher inflation would argue for a firmer stance. At the same time, weaker growth would pull in the opposite direction, particularly if the drag on activity proves persistent. Bloomberg Economics estimates that if Brent crude continues to price at around $80 barrel for an extended period, it could add 0.5pp to Eurozone inflation and shave 0.3pp from economic growth.

Much depends on how long the conflict persists in the region and whether energy price pressures become more entrenched.

Source: Bloomberg, BIL

Eurozone unemployment rate falls to all-time low in January

The seasonally-adjusted unemployment rate in the Eurozone edged down to 6.1% in January from 6.2% the month prior, below expectations and to an all-time low. Youth unemployment also fell, decreasing from 15% in December to 14.8% in January.

Among the bloc’s largest economies, Germany and the Netherlands recorded the lowest jobless rates at 4%, while Spain, France, and Italy saw the highest at 9.8%, 7.7% and 5.1% respectively.

Despite the fact that the labour market has gone from being a shock amplifier to a shock absorber, consumer activity remains weak for the time being. Eurozone retail sales fell 0.1% MoM in January, after an upwardly-revised 0.2% gain in December.

US data points to strengthening business activity

Source: ISM, Bloomberg, BIL

According to the ISM reading, the US services sector is now expanding at the fastest pace since August 2022. The PMI hit 56.1, up from 53.8 in January, with business activity ramping up to levels unseen since September 2024. New orders rose at the briskest pace seen in 17 months, and employment growth hit a 12-month high. Prices cooled slightly but the index remained above 60, indicating continued cost pressures.

Activity in the Manufacturing sector slowed, after expanding at the fastest pace since 2022 in January. The headline PMI slipped only slightly, however, from 52.6 to 52.4, signaling a second consecutive month of expansion. New orders remained strong after a blistering start to the year (55.8 from 57.1), and the contraction in employment became less pronounced (48.8 from 48.1). Price pressures heated up, with the subindex reaching the highest level since June 2022 (70.5(!) from 59), This was largely driven by cost increases for steel and aluminum, as well as tariffs applied to various imported goods.

The Fed’s Beige Book, also released last week, embellished the idea that the US economy remains on stable footing, with activity increasing at a slight to moderate pace in eight districts, while three reported no change and one a decline. The document, which gathers anecdotal evidence on economic conditions, also highlighted that inflation remains a concern. Nine districts specifically cited tariffs as a factor for higher non-labour input costs, which include energy, insurance, and raw materials.

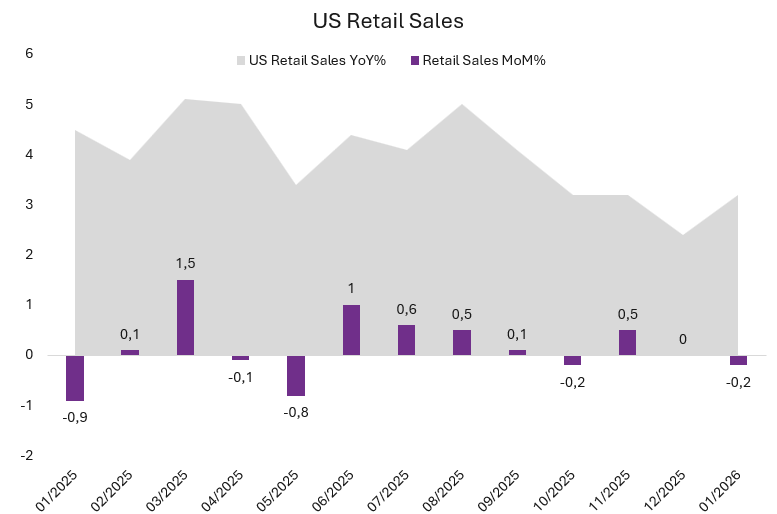

US consumers pull back on spending with the labour market still in limbo

Source: Bloomberg, BIL

While the engines of the corporate sector may be revving up, consumer activity softened in January. Retail sales fell 0.2% month-on-month, slightly above expectations for a 0.3% decline. This was partly due to severe weather, particularly Storm Fern which hit on January 23 and disrupted spending at food and drinking places, and at brick-and-mortar stores, to the benefit of online retailers.

Volumes fell sharply for motor vehicle and parts dealers (-0.9%), gasoline stations (-2.9%), electronics and appliances stores (-0.6%), and clothing & accessories (-1.7%). On the other hand, they rose for furniture (0.7%), building materials and garden equipment (0.6%), miscellaneous stores (2%), and non-store retailers (1.9%).

Control group sales, which are used in the GDP calculation, rose at a still-decent clip of 0.3%. Year-on-year retail sales remain relatively strong at 3.2%.

The future path of consumption now depends on the labour market.

On that front, Friday’s nonfarm payroll report didn’t bring good news, revealing a 92,000 decline in payrolls, the weakest reading in four months and a sharp reversal from January’s 126,000 gain. Much of the weakness came from sector‑specific disruptions, including a 28,000 drop in healthcare employment, partly due to the Kaiser Permanente strike, along with declines in IT (-11k), federal government (-10k), transportation and warehousing (-11k), and manufacturing (-12k). Some of these losses may have been due to inclement weather.

The unemployment rate ticked up to 4.44%, while average hourly earnings grew 3.8% year over year, slightly above January’s 3.7% pace, signaling that wage pressures remain firm despite the softer headline payroll figure.

Following the release of the data, hopes that the labour market is turning a corner appeared to be dashed. Markets continued to price in two Federal Reserve rate cuts this year, but macro data is out of focus for the time being as markets focus on ongoing events in the Middle East.

China sets its lowest growth target since 1991

China has set its 2026 GDP growth target at 4.5-5%, the lowest since 1991, as it pivots toward what policymakers describe as “quality-first” growth amid persistent deflationary pressures and unresolved trade tensions with the US.

Even though China’s export sector remains substantial, posting a record $1.2 trillion surplus in 2025, it is becoming a less reliable growth engine in an increasingly fragmented world. Exports to the US plunged by around 20% last year, as the two countries unleashed a series of retaliatory tariffs on one another. In October, both sides agreed to a one-year pause in their trade war, and fresh negotiations are expected during President Trump’s planned visit to Beijing on March 31st.

For obvious reasons, internal economic resilience is becoming ever more crucial for leaders in Beijing. This week, the Government released a draft of the 15th Five‑Year Plan (2026–2030), which will be formally approved this week. The plan places heavy emphasis on boosting household consumption, strengthening innovation capacity, and expanding high‑tech and advanced manufacturing, reaffirming China’s long‑term goal of technological leadership and supply‑chain dominance.

At the same time, Beijing has announced a 7% increase in defense spending for 2026, the smallest rise in five years but still significant as China navigates heightened regional and global tensions.

Calendar for the week ahead

Monday – China National People’s Congress, Inflation data (February). Germany Industrial Production (January). US Consumer Inflation Expectations (February).

Tuesday – China National People’s Congress, Balance of Trade (Jan-Feb). Germany and France Balance of Trade (January). US Existing Home Sales (February), NFIB Small Business Optimism (February).

Wednesday – China National People’s Congress. Germany Inflation (Final, February). Spain Retail Sales (January). US Inflation (February). OPEC Monthly Report.

Thursday – US Housing Starts and Building Permits, Jobless Claims.

Friday – UK Industrial Production, GDP (January). France and Spain Inflation (Final, February). Eurozone and Italy Industrial Production (January). US PCE Inflation (January), Personal Income and Spending, Durable Goods Orders, JOLTs Job Openings (January), Michigan Consumer Sentiment (Preliminary, March).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

April 20, 2026

Weekly Investment Insights

Market Snapshot On Friday, equity markets celebrated the opening of the Strait of Hormuz to commercial shipping during the ceasefire. US equity markets posted strong...

April 13, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Last week, oil prices slumped and equities rallied after the US and Iran agreed a two-week ceasefire. However, hopes for de-escalation were quickly...

April 13, 2026

BILBoardBILBoard April 2026 – Through the noise

Based on the Asset Allocation Committee on March 31 2026 Geopolitical uncertainty took centre stage in March as the conflict in the Middle East extended...

April 8, 2026

FocusMissing the Market’s Best Days: Why S...

Key takeaways: Missing the market’s best days can significantly reduce long-term returns The best days often occur in periods of stress rather than stability Staying...

March 30, 2026

Weekly InsightsWeekly Investment Insights

Kindly note that our Weekly Insights will pause over the upcoming bank holiday weekend. Market Snapshot The conflict in the Middle East has now extended...