BIL INVESTMENT INSIGHTS

Market Snapshot

Oil prices surged above $126 per barrel on Thursday, reaching their highest level since the conflict in the Middle East began, as markets grew increasingly concerned that hostilities could be prolonged after President Trump told oil executives that the blockade of the Strait of Hormuz could last for months. Prices later reversed course, however, falling by more than $13 on the same day as traders reassessed demand fundamentals and the availability of physical barrels. This morning, Brent crude is trading around $109 per barrel.

On Tuesday, the United Arab Emirates announced its decision to exit OPEC, a move that represents a significant setback for the oil cartel and its de facto leader, Saudi Arabia. The departure will grant the Gulf state greater autonomy over its production strategy and export volumes. The UAE has indicated plans to gradually increase output; prior to the closure of the Strait of Hormuz, the country was already maxing out its OPEC quota of approximately 3.6 million barrels per day.

The abrupt exit is likely to weaken the cohesion of the organisation, which coordinates member countries’ production levels to influence global oil prices. The UAE is OPEC’s third‑largest producer, behind Saudi Arabia and Iraq, and its decision comes at a time when fracking is allowing the US to capture an increasing share of the global market.

While the closure of the Strait of Hormuz is currently eclipsing most factors driving the oil price, the UAE’s exit from OPEC could make oil prices more volatile over the longer term.

The oil cartel met over the weekend and agreed to a further increase in production quotas of 188,000 barrels per day by easing some of its previous output cuts. However, the decision is widely viewed as symbolic, as several member countries currently lack the capacity to significantly raise production due to damage to production facilities or constraints on exporting additional supply through the Strait of Hormuz.

Trade tariffs also became a topic again after President Trump threatened a 25% levy on EU cars and trucks, claiming that the bloc is not fully complying with the terms laid out in a deal struck last July. In response, Eurogroup President Kyriakos Pierrakakis said that the bloc seeks dialogue, but that if there is a deviation from what was previously agreed, “all options are on the table and all choices will be on the table.” The latest move from the White House adds further doubt in a global economy already fraught with uncertainty stemming from the standoff in the Strait of Hormuz.

Turning to corporate earnings, US companies have reported their strongest results since the fourth quarter of 2021, led by robust growth in the technology sector. Strong earnings momentum helped push equity markets higher, largely offsetting negative sentiment stemming from the conflict in the Middle East and ongoing volatility in oil prices.

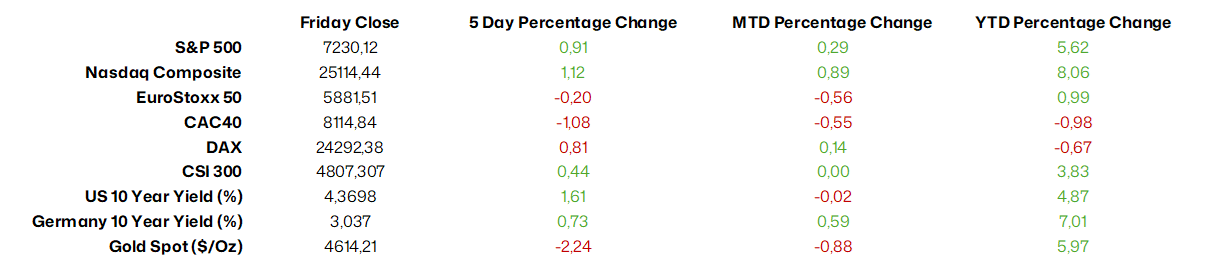

Source: Bloomberg, BIL as of May 4

Macro Snapshot

Fed holds rates steady amid raising energy prices

The Federal Reserve kept its benchmark federal funds rate unchanged at 3.5%–3.75% for a third consecutive meeting on Wednesday, though the decision revealed some internal divisions. Three FOMC members supported leaving rates unchanged but opposed language in the statement suggesting a potential bias toward lowering borrowing costs at upcoming meetings. In addition, one official voted to cut interest rates by 25 basis points. Together, the four dissenting votes marked the first time since 1992 that such a number of policymakers have broken with the consensus.

In explaining its decision, the Fed pointed to continued weakness in job growth and persistently elevated inflation, partly driven by sharp increases in global energy prices. The central bank highlighted heightened uncertainty, noting that “developments in the Middle East are contributing to a high level of uncertainty about the economic outlook.”

The central bank reiterated its commitment to a data-dependent approach, emphasizing that it will continue to assess incoming economic information, the evolving outlook, and the balance of risks when determining the future stance of monetary policy.

Wednesday’s meeting also marked the final one chaired by Jerome Powell. Kevin Warsh is set to assume the role of Fed chair in mid-May. Powell announced that he intends to remain on the Board of Governors “for a period of time” after stepping down as chair. This implies that Stephen Miran, who has dissented at every meeting since he joined the Fed board in September, will have to vacate his seat. Miran is currently on leave from his White House role advising Trump on the economy, and has advocated for steep rate cuts.

ECB holds rates at 2% as growth cools and inflation heats up

As expected, the European Central Bank kept its key interest rate unchanged at 2% at its April meeting, a level maintained since June 2025.

Policymakers indicated that they need more time to evaluate the economic impact of the ongoing conflict in the Middle East and thus provided no forward guidance. Rather, the ECB reiterated its data-dependent approach and its commitment to deciding policy on a meeting-by-meeting basis.

In its statement, the Governing Council acknowledged a more challenging outlook, warning that “upside risks to inflation and downside risks to growth have intensified,” while maintaining that it remains “well positioned to navigate the current uncertainty.” It also cautioned that a prolonged conflict and persistently elevated energy prices could have a broader impact on both inflation and economic activity.

Recent data releases already point to a weakening economic environment.

Growth has slowed, with Eurozone GDP rising just 0.1% quarter-on-quarter in Q1 2026, down from 0.2% previously and below expectations. The slowdown was largely attributed to the war in the Middle East which has halted flows of oil, its byproducts, and liquified natural gas.

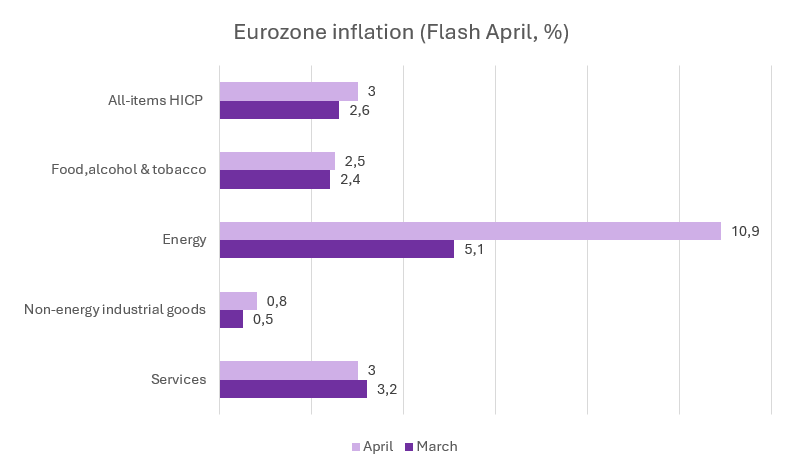

The inflationary pressure stemming from the conflict was also evident in the latest consumer price data; headline inflation increased to 3.0% YoY in April from 2.6% in March. Energy prices were the main driver, surging 10.9%, the fastest pace since February 2023. Inflation also accelerated in non-energy industrial goods and for food, alcohol and tobacco. By contrast, services inflation showed signs of easing.

Core inflation, which excludes volatile items such as food and energy, edged lower to 2.2% from 2.3% in the previous month.

The ECB’s latest bank lending survey shows financial conditions in the Eurozone have tightened following the escalation in geopolitical tensions.

Source: Eurostat, BIL

The Bank of England leaves rates unchanged

The Bank of England (BoE) kept interest rates on hold last week at 3.75%, but signalled that further tightening may be necessary if the conflict in the Middle East persists and the global energy shock deepens. The decision was nearly unanimous, with all but one member of the Monetary Policy Committee voting to hold rates steady; one member dissented in favour of an immediate quarter-point increase. Nevertheless, the minutes of the meeting showed that the committee was heavily divided, with some members preferring to act early, while others wanted to wait for further evidence before changing policy.

Before the escalation of the conflict in the Middle East, markets had expected the BoE to reduce interest rates as inflationary pressures eased and economic growth remained weak. However, the outlook for monetary policy has shifted as higher energy prices have begun to feed into UK inflation.

Speaking at a press conference following the decision, BoE Governor Andrew Bailey said, “We’ll continue to monitor the situation and its impact on the UK economy very closely. Whatever happens, our job is to make sure that inflation gets back to the 2 % target after the initial impact of the war on energy prices has passed”, a comment that was interpreted as relatively dovish.

In response, market participants scaled back expectations of further tightening, with the probability of a quarter-point rate hike in June falling to around 50%, down from roughly 70% before the announcement.

Calendar for the week ahead

Monday – Switzerland Manufacturing PMI (April). Eurozone Manufacturing PMI (Final, April). US Factory Orders (March).

Tuesday – Switzerland Inflation (April). US Balance of Trade (March), Composite & Manufacturing PMI (Final, April), ISM Services PMI (April). JOLTs Job Openings (March).

Wednesday – Eurozone Composite & Services PMI (Final, April).

Thursday – Switzerland Unemployment Rate (April). Eurozone Retail Sales (March). US Challenger Job Cuts (April), Jobless Claims.

Friday – Germany Industrial Production (March). Switzerland Consumer Confidence (April). US Non Farm Payrolls (April), Unemployment Rate (April), Michigan Consumer Sentiment (Prel, May).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

June 19, 2026

Weekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...

June 16, 2026

BILBoardBILBoard Mid-Year 2026 – In sea...

Sunday, 21 June marks the official start of summer here in the northern hemisphere. Yet, after an unseasonably warm spring, conditions have turned cooler and...

June 15, 2026

Weekly InsightsWeekly Investment Insights

Written as of 15 June, After a volatile week, major US equity indices ended higher on Friday, supported by growing optimism around a potential...

June 5, 2026

Weekly InsightsWeekly Investment Insights

Written as at 5 June 2026 The record-breaking streak among chipmakers paused on Thursday after the outlook from a prominent player cast some doubt...

June 1, 2026

Weekly InsightsWeekly Investment Insights

Written as of 1 June 2026 US stock indices recorded new highs last week with investor optimism around AI serving as the driving force....