BIL INVESTMENT INSIGHTS

Expectations for monetary policy easing by the US Federal Reserve (Fed) have shifted significantly since the start of the year. The conflict in the Middle East, and the sharp rise in global energy prices that followed, has pushed inflation expectations higher and forced markets to reassess the likely path for interest rates.

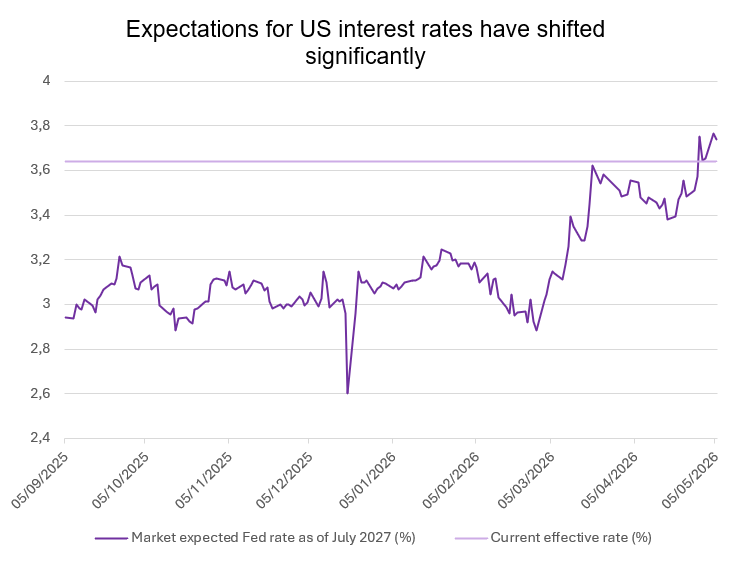

Source: Bloomberg, BIL

Before the conflict began, market participants expected the US central bank to lower interest rates by a total of 50 basis points in 2026, which would have brought the funds benchmark rate to 3% - 3.25%. Since then, however, markets have sharply pared back those expectations. Traders now see little chance of easing this year, with some even beginning to price the risk of further tightening in 2027.

Some comments from the Federal Open Market Committee (FOMC) support this. At its latest meeting, the committee voted to keep rates on hold at 3.5%–3.75% for a third consecutive meeting, though the group appeared more divided on what guidance should be given on future moves. Three policymakers supported leaving rates unchanged but opposed language in the statement suggesting a potential bias toward lowering borrowing costs at upcoming meetings. Fed Chair Jerome Powell also struck a more hawkish tone, indicating that the Fed’s “easing bias” might come to an end as soon as the June meeting. In response, benchmark 10-year Treasury yields have risen to around 4.33% from 3.94% before the war began, while rate-sensitive 2-year yields have increased to around 3.84% from 3.37%, reflecting market participants digesting the reality of “higher-for-longer” interest rates.

Inflation has become the main risk

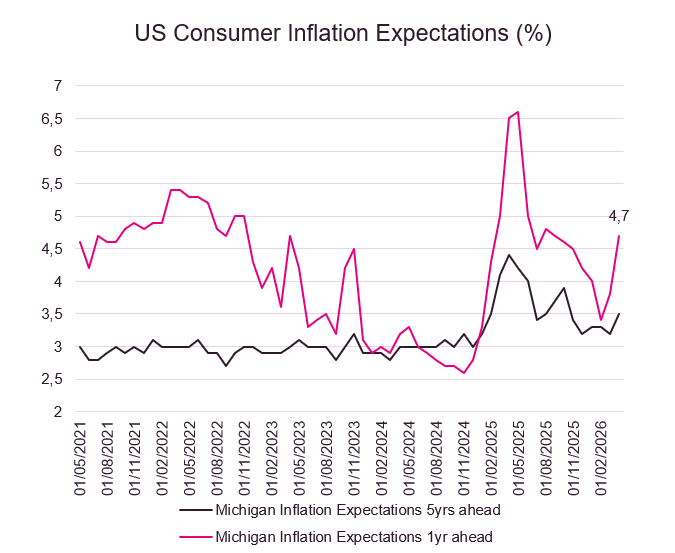

The primary driver behind this repricing has been the resurgence of inflation risk linked to the conflict in the Middle East. Despite the US’ relatively strong position as a net energy exporter, soaring global energy costs have started to feed into consumer prices in the US. Household budgets are coming under pressure, with the average price for fuel around $4.50 a gallon, a four-year high. This is clearly a concern for consumers, whose inflation expectations have risen significantly since the conflict began.

Source: Bloomberg, BIL

Companies are also beginning to signal renewed pricing pressure. An increasing number of firms have referenced price increases, or the likelihood of them, in recent earnings releases. With the last inflation surge still fresh in memory, businesses could act quicker this time to protect margins by passing higher input costs on to consumers.

Despite higher fuel prices, US consumers have continued to spend. In fact, US retail sales rose to a one-year high in March, largely driven by a 15.5% jump in gas station receipts, as costs were pushed higher. Even excluding fuel, spending remained broadly firm, supported in part by larger‑than‑usual tax refunds received this year, which provided a temporary boost to household cash flows.

However, it is also worth noting that higher interest rates generally act as a brake on stock markets, which could reduce spending among the wealthiest households, who are sensitive to fluctuations in share prices.

The key question is how long consumers can continue to absorb higher prices if energy costs remain elevated and if the "Wealth Effect" is in jeopardy. Even if the conflict was resolved in the near future, allowing oil prices to stabilise around pre-conflict levels, inflation concerns are unlikely to dissipate quickly, given that price pressures were already building before the conflict began.

Growth holding up

At the same time, relatively robust economic growth and a resilient labour market have shifted the policy focus away from providing stimulus and toward managing inflation risks. Labour market data for March surprised strongly to the upside, suggesting employment is stabilising even without rate cuts. Economic growth also regained momentum in the first quarter, supported by increased investment in artificial intelligence and a rebound in government spending following last year’s shutdown.

This resilience has somewhat narrowed the Fed’s room for manoeuvre. Strong employment, solid investment activity and continued consumer spending make it difficult for policymakers to look through the current inflation shock. Without clear evidence of labour‑market deterioration, rate cuts are hard to justify, even if geopolitical risks fade or energy prices stabilise.

A shift towards higher-for-longer

As a result, expectations for US monetary policy have moved decisively toward a higher‑for‑longer outcome. What began the year as a debate over the timing and extent of rate cuts has evolved into a discussion about how long the Fed can remain on hold, and whether further tightening might yet be required should inflation pressures persist.

While persistent cost pressures may eventually weigh on demand and shift risks toward a growth slowdown, the near‑term balance continues to favor policy restraint over easing. Markets have therefore been forced to adjust not only to fewer expected rate cuts, but to the possibility that none at all may materialize, with some even beginning to consider renewed tightening.

This delicate balancing act comes at a moment of significant change within the Federal Reserve itself. April’s meeting marked Jerome Powell’s final one as chair, with Kevin Warsh set to assume the role in mid‑May. While Warsh is widely expected to take a more dovish approach to monetary policy, Powell’s decision to remain on the Board for “a period of time” implies a shifting internal balance, including the departure of persistent dissenter Stephen Miran, who has argued for aggressive rate cuts.

Against this backdrop, the Fed’s likely course is one of caution. For now, resilient growth keeps policy on hold. But the longer elevated costs weigh on confidence and demand, the greater the risk that today’s inflation challenge gives way to a potential growth slowdown.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

July 27, 2026

Weekly Investment Insights

As anticipated in last week's note, the expiry of Section 122 tariff measures on 24 July was followed by the announcement of a new round...

July 17, 2026

BILBoardBILBoard July 2026 – A false dawn

Based on decisions taken at the July 6 Asset Allocation Committee Just a few weeks ago, it appeared that the worst of the Middle East...

July 17, 2026

Weekly InsightsWeekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 17, 2026

Weekly InsightsWeekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 13, 2026

Weekly InsightsWeekly Investment Insights

Geopolitical tensions returned to the forefront of financial markets last week. After tankers were reportedly targeted in the Strait of Hormuz, the US launched...