BIL INVESTMENT INSIGHTS

Based on decisions taken at the July 6 Asset Allocation Committee

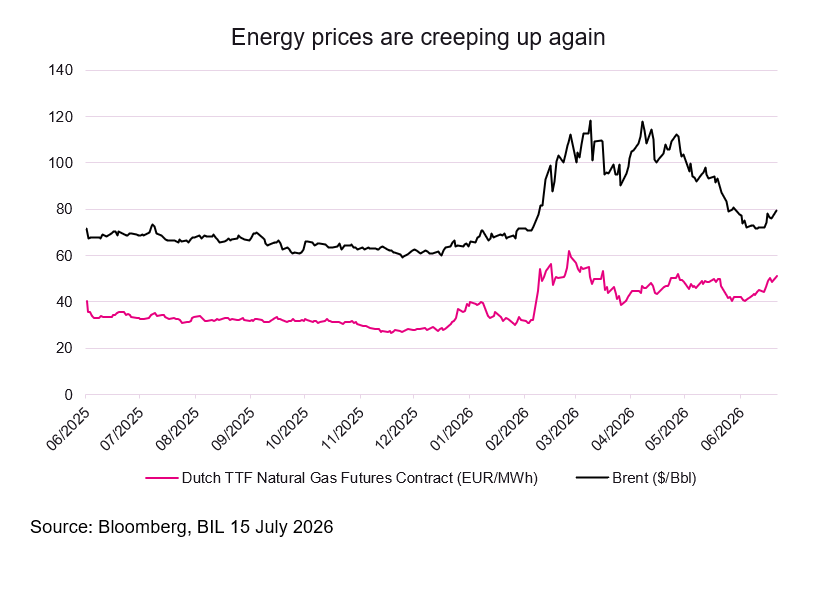

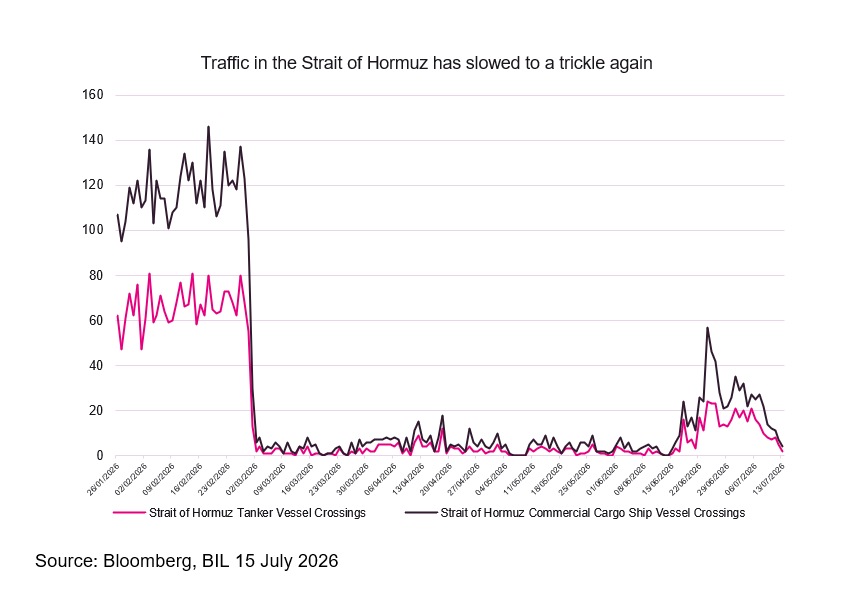

Just a few weeks ago, it appeared that the worst of the Middle East crisis was behind us. After a peace agreement was signed between the US and Iran on 17 June, it was tempting to look past the prospect of a prolonged energy supply shock. Indeed, traffic in the Strait of Hormuz was beginning to pick up, Brent crude prices had fallen to around USD 71 per barrel, and headline inflation was starting to cool.

Investors, corporates and consumers responded positively. Sentiment indicators improved and markets increasingly priced a return to a more benign macroeconomic environment.

It now appears that this optimism was premature.

Diplomatic efforts have been complicated by diverging objectives. The Trump administration is keen to restore normal shipping flows through the Strait of Hormuz in order to ease energy market pressures ahead of the US midterm elections. Iran, meanwhile, remains reluctant to relinquish leverage over one of the world's most strategically important waterways. Tensions escalated once again on 7 July, when the US launched strikes against Iranian targets following attacks on vessels transiting the Strait.

Since then, hostilities have continued and activity through the Strait has slowed sharply once more. Brent crude has climbed above USD 85 per barrel, while European benchmark gas prices have risen by more than 20%. Insofar as now, these moves are considered orderly and suggest that markets are pricing a bottleneck rather than a severe supply shortage. Nevertheless, they serve as a reminder that geopolitical risks remain elevated and that energy-related disruptions are still a feature of the macro backdrop.

Macroeconomic Overview

The global economy remains caught between two powerful forces: war and technology.

On one hand, geopolitical tensions, higher energy prices and inflation risks are weighing on growth prospects. On the other, unprecedented investment in artificial intelligence continues to support economic activity, corporate earnings and productivity expectations.

On a country-by-country basis, exposure to these themes varies, creating bifurcated economic expectations. Energy-exporting countries are benefiting from higher commodity prices and improved terms of trade, while economies closely linked to the AI investment cycle continue to attract capital and demonstrate greater resilience. Conversely, energy-importing countries with limited exposure to AI profit pools face a more challenging environment.

The US remains uniquely positioned. It is both a net energy exporter and the global centre of AI investment. Estimates suggest that the largest hyperscalers could spend as much as USD 820 billion in 2026 alone. Consumer spending also remains resilient, supported by a stabilising labour market.

While we remain constructive on AI as a long-term theme, we see potential near-term risks to the investment cycle. Additional semiconductor manufacturing capacity is expected to come online over the coming quarters, potentially coinciding with a moderation in hyperscaler capex growth. At the same time, competition is intensifying as China accelerates efforts to achieve greater self-sufficiency in advanced technologies.

Moreover, many of the companies expected to benefit most from AI are becoming increasingly cost-conscious, or realizing that adapting their systems, processes and data infrastructure to fully capture AI-related productivity gains may take longer than initially anticipated.

The Q2 earnings season will therefore be critical in assessing whether elevated investment levels are translating into stronger revenues, expanding margins and sustainable cash-flow growth.

The principal macroeconomic risk facing markets, however, may be Federal Reserve tightening. The hawkish tone adopted by the new Chair Kevin Warsh surprised investors and reinforced concerns that the Fed may be willing to tighten policy in the near-term. However, the benign June inflation report, with CPI falling 0.4% month-on-month in its first decline since 2020, may allow policymakers to talk hawkish talk without walking a hawkish walk. Much will depend on developments in energy markets and the extent to which second-round inflation effects emerge.

The Eurozone economy remains more subdued. Renewed geopolitical tensions are likely to weigh disproportionately on Europe given its dependence on imported energy. While headline inflation in the currency union has receded, wage pressures, and ongoing energy-related uncertainties suggest the ECB may not be ready to declare victory just yet. As a result, the possibility of further policy tightening later this year cannot be ruled out.

Investment Decisions

Against a backdrop of geopolitical uncertainty, persistent inflation risks and increasingly concentrated equity markets, we have made several adjustments intended to improve diversification, and position portfolios for a broader range of outcomes.

Firstly, we increased exposure to European equities. This is a tactical play, as we believe that any signs of progress in Middle East discussions, could bring tailwinds.

We also reallocated part of our US investment-grade bond exposure into European inflation-linked government bonds. Real yields were close to their highest levels in 15 years, offering an attractive entry point, while optimism around a lasting peace in the Middle East had driven European inflation expectations sharply lower. With breakeven rates effectively pricing inflation below the ECB’s 2% target, we viewed the market’s assumptions as overly optimistic. Subsequent developments have validated the prudence of that positioning.

Within Emerging Market debt, we reallocated part of our exposure from hard-currency bonds into local-currency. Hard-currency EMD has delivered a strong performance in recent quarters, reducing valuation appeal and limiting the potential for further spread tightening. While the overarching case for Emerging Market bonds – built upon resilient macro fundamentals and attractive carry - remains intact, we now believe that unhedged local-currency debt currently offers the most effective way to express a positive view - even in an environment where the Fed remains relatively hawkish.

We also upgraded Financials from neutral to positive. Entering the second-quarter earnings season, we expected trading and investment-banking revenues to exceed guidance, and early results have broadly confirmed that view. Heightened market volatility and robust client activity across both equity and fixed-income markets have supported trading income and contributed to earnings surprises across a number of major banks. Beyond this short-term earnings momentum, the sector continues to benefit from improving capital-markets activity, growing investment-banking pipelines and the prospect of a gradual recovery in M&A. Net interest income is improving, while balance sheets remain healthy and credit quality remains strong.

Finally, given the strength of the US economy, ongoing labour market resilience and a Fed that is clearly cautious on inflation, we felt comfortable reducing the level of currency hedging on our US dollar exposure.

Conclusion

The period immediately following the US-Iran peace agreement encouraged markets to price a return to normality. Recent events have demonstrated how fragile that assumption was. Geopolitical tensions remain elevated and inflation pressures have not disappeared. At the same time, investors are increasingly questioning whether today's elevated AI-related spending will ultimately translate into the earnings growth that markets currently expect.

While we remain constructive on risk assets and continue to view artificial intelligence as one of the most powerful long-term investment themes of the coming decade, we believe the next phase of the cycle is likely to reward diversification, valuation discipline and a helping of inflation protection.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

July 17, 2026

Weekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 17, 2026

Weekly InsightsWeekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 13, 2026

Weekly InsightsWeekly Investment Insights

Geopolitical tensions returned to the forefront of financial markets last week. After tankers were reportedly targeted in the Strait of Hormuz, the US launched...

July 6, 2026

Weekly InsightsWeekly Investment Insights

Central bank communication was a key market driver last week, with several officials taking the mic. Stateside, Richmond Fed President Tom Barkin warned that US...

June 19, 2026

Weekly InsightsWeekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...