BIL INVESTMENT INSIGHTS

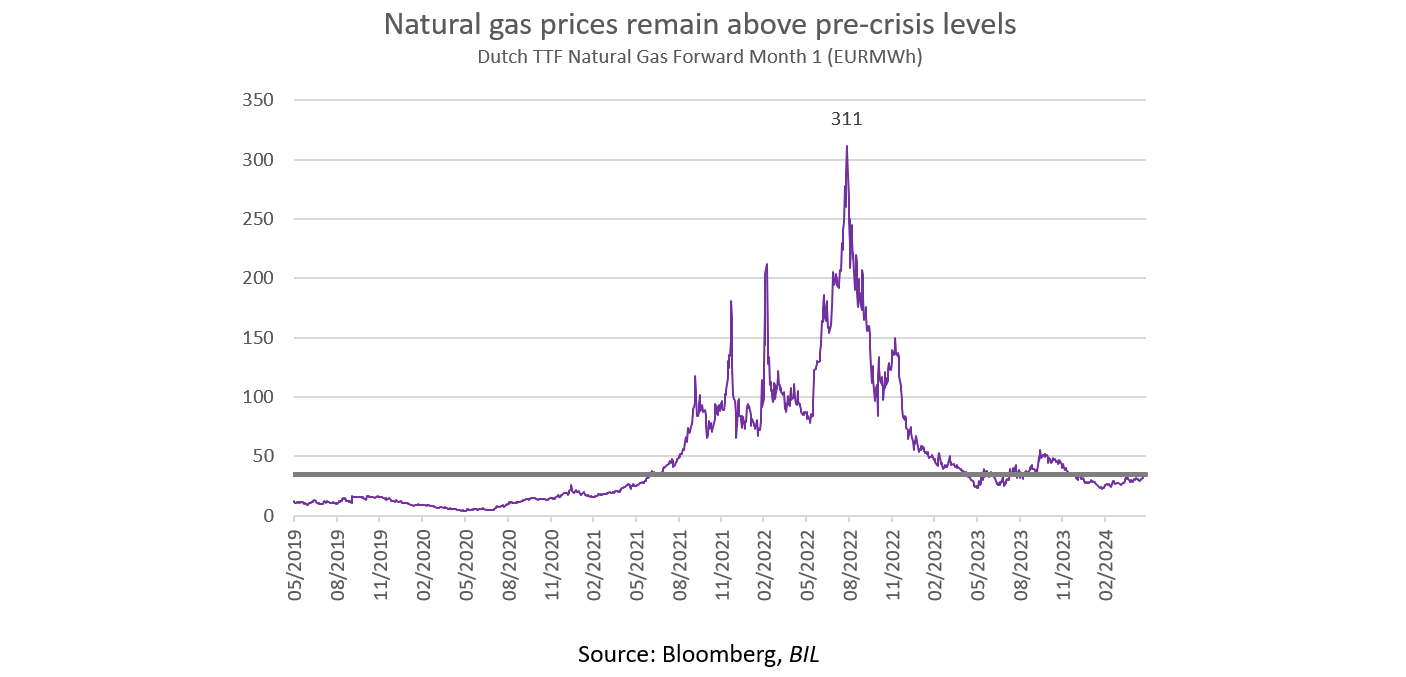

Prior to the invasion of Ukraine in February 2022, the lion’s share of Europe’s energy imports came from Russia. It accounted for 28% of the continent’s total crude oil imports, while Russian pipelines delivered 44% of all imported gas. The outbreak of war and the subsequent sanctions therefore resulted in a huge supply shortfall and a global market shock that sent prices skyward. In the aftermath, wholesale gas prices rose tenfold, while crude rose above 120 USD/bbl.

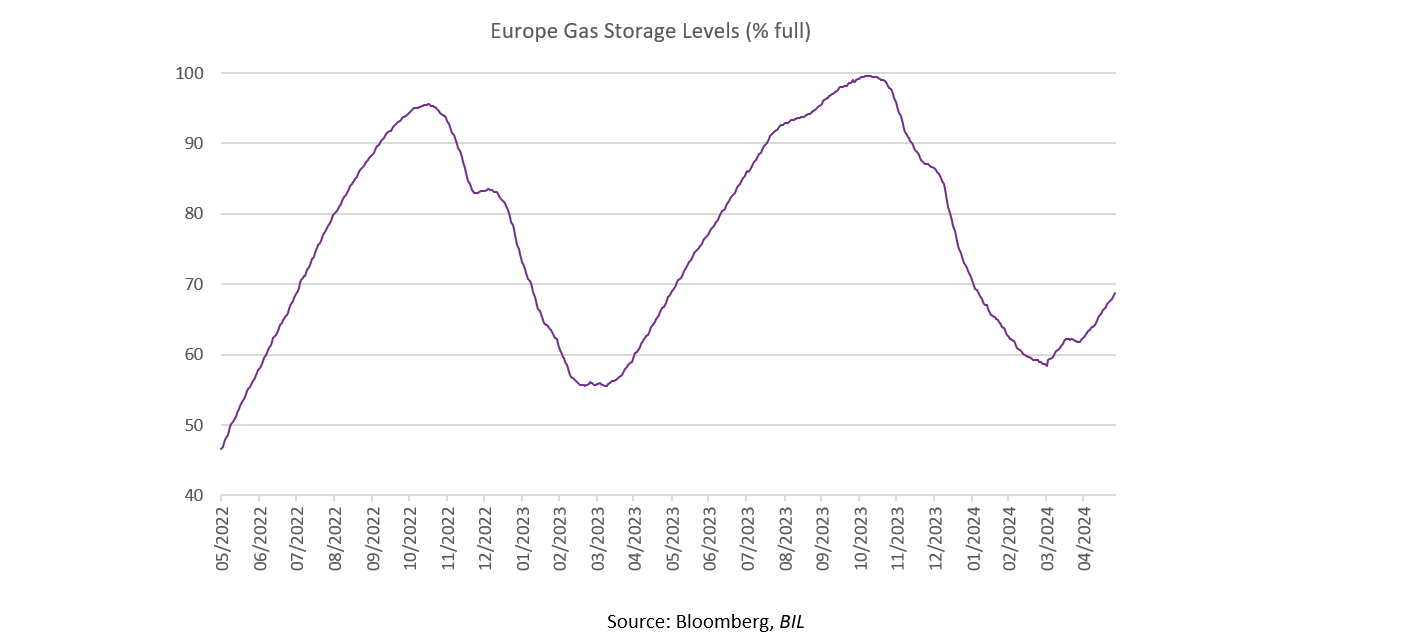

Fast forward to today, there are clear signs that Europe’s energy crunch is easing. For example, just two years on, the continent has emerged from winter 2023-24 with gas storage at record-high levels (59% full), while wholesale prices have come down substantially. Current dynamics suggest the EU will meet its target to fill facilities to 90% well ahead of the November deadline. Despite ongoing geopolitical tensions, the price of crude has also eased, and currently trades at around 80 USD/bbl.

Various factors have led to the amelioration of Europe’s energy situation.

The first might be considered luck: exceptionally mild weather.

At least when it comes to gas, the second factor is a fall in demand. Last year, European countries consumed 20% less natural gas relative to the average recorded across 2019-2021.[1] Industrial demand has been particularly depressed and has not yet shown signs of recovering, despite a decline in wholesale gas prices. Household demand is more volatile; it is very seasonal with gyrations in demand driven by temperatures.

The third key factor is reactivity on the part of policymakers to secure alternative energy sources.

In the past, European countries mainly relied on piped gas to satisfy their needs and absorbed excess supply from the global liquefied natural gas (LNG) market when the price was right. Today, Europe has joined the likes of China and Japan to become a major LNG importer, with its imports surging by almost 60% YoY in 2022 alone. This has involved significant investments to expand regasification infrastructure which will allow the EU to further tap the LNG market in the future. Germany, which had no LNG terminal until late- 2022, has outlined plans to build several such facilities.

In terms of the origins of that gas, the US has emerged as Europe’s primary supplier. While total US LNG exports expanded by just 10% in 2022 due to supply constraints, flows towards Europe more than doubled (+140%).

Looking at oil, the decrease of crude imports from Russia was compensated by increased imports from traditional partners like Saudi Arabia, the US and Norway, as well as less traditional suppliers like Brazil and Angola.

Nuclear has also played a role in filling the supply gap. In 2023, France (Europe’s biggest nuclear power operator with 56 reactors), became a net exporter of electricity. This summer, its first new reactor in 25 years is scheduled to be connected to the grid in Normandy, and the country plans to build at least six new reactors in the late 2030s (though a skills shortage is a potential obstacle to these ambitions).

In the short-term, these factors combined have helped Europe avert the worst-case scenario of a severe energy shortage leading to extreme measures like rationing.

Fragilities remain

However, looking at the bigger picture, Europe’s energy situation is far from comfortable. It must now rely on global energy markets which are vulnerable to supply shocks, or even perceived threats of them.

Perhaps the most obvious threat today is the fraught geopolitical landscape.

Due to attacks in the Arabian Peninsula, for several months, tankers carrying fuel products between the Atlantic and Pacific basins have had to take a costly detour around the horn of Africa. This is leading to a fragmented global marketplace whereby traders are pairing shipments with destinations that are geographically close (e.g., US imports are being directed towards Europe and Middle Eastern exports towards Asia). These efforts will likely intensify when fuel demand mounts ahead of winter, when shipping costs usually also rise. Such fragmentation will make it more difficult to divert supply between regions if there is an outage at an export plant, a sudden surge in demand, or an unforeseen event (like the recent drought in the Panama Canal).

Also worth noting is the fact that European wholesale gas prices are still almost double their pre-crisis levels, which is tangibly impacting the competitiveness of Europe’s energy-intensive industries. Ironically, the recent softening we have seen in energy prices is due to muted demand stemming partly from the energy crisis itself. A rebound of the European economy, particularly industrial powerhouses like Germany, could therefore reinforce a feedback loop.

Lastly, an uptick in Chinese activity would signal the return of a significant LNG market buyer, again potentially pressuring prices upwards and highlighting Europe’s dependence on more expensive sources.

A coordinated approach

Insofar as now, Europe’s band-aid fixes to the energy crisis have proven highly effective, but the ultimate cure - reducing the level and volatility of energy prices in European wholesale markets - could be years in the making. That solution will be multi-faceted and will require coordinated policies, with the EU leaning on its strength as an economic bloc. One part of it might entail pooling demand and then getting involved in the commercial negotiations to strike long-term deals that offer suppliers a predictable revenue stream while ensuring gas security and affordability to European countries. Another part will clearly have to focus on increasing domestic supply, most likely through accelerated investment in alternatives.

[1] https://www.bruegel.org/dataset/european-natural-gas-demand-tracker#:~:text=Compared%20to%20the%20average%20across,the%20Baltic%20states%20and%20Finland.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

July 17, 2026

BILBoardBILBoard July 2026 – A false dawn

Based on decisions taken at the July 6 Asset Allocation Committee Just a few weeks ago, it appeared that the worst of the Middle East...

July 17, 2026

Weekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 17, 2026

Weekly InsightsWeekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 13, 2026

Weekly InsightsWeekly Investment Insights

Geopolitical tensions returned to the forefront of financial markets last week. After tankers were reportedly targeted in the Strait of Hormuz, the US launched...

July 6, 2026

Weekly InsightsWeekly Investment Insights

Central bank communication was a key market driver last week, with several officials taking the mic. Stateside, Richmond Fed President Tom Barkin warned that US...