BIL INVESTMENT INSIGHTS

Around Thanksgiving, a Wall Street blogging site started selling Christmas sweaters with the slogan “Inflation is Transitory, Happy Holidays from the Federal Reserve”. Those who purchased the jumper now have a stranded asset on their hands as the message is very much out-of-date, demonstrating how quickly the Fed’s hawkish pivot came about.

For months, the Fed clung to the notion that pandemic-induced price pressures would come down on their own accord. This was repeatedly challenged by markets and dissident voices were emerging even from within the Fed itself. Atlanta Fed president Raphael Bostic admitted in October that he had swear jar in his office – rather than being associated with curse words, staffers (and Bostic himself) were to put a dollar in every time they used the word "transitory." Through fall, red-hot inflation showed no signs of cooling; after 5 months at 5% or above, headline CPI came in at 6.2% in October, before hitting a 39-year high of 6.8% in November. With inflation broadening out and wages rising at their fastest pace “in many years”, pressure mounted on the Fed to get a handle on prices. At his testimony before Congress on November 30th, the Chair Jerome Powell, finally dropped the word “transitory” from his inflation vocabulary. Then, at its December meeting, the Fed walked the talk and changed its policy stance from dovish to decidedly hawkish, in order to regain control of inflation and the narrative surrounding it.

Acknowledging that it’s inflation mandate had been satisfied and that the “risk of higher inflation becoming entrenched has increased”, the Fed announced that it would double its pace of tapering from $15bn to $30bn per month, indicating that asset purchases should draw to a close completely by mid-March.

The earlier exit from quantitative easing gives the Fed more flexibility to raise rates sooner to rein in inflation. Powell was clear that with a strong growth outlook, a rapidly improving labour market and well above target inflation, the distance between ending QE and a rate lift-off could be very short. On the labour market, the unemployment rate has plunged to 4.2%, the lowest level since the pandemic began, and Powell noted that recent improvements “have narrowed the difference in employment across groups”.

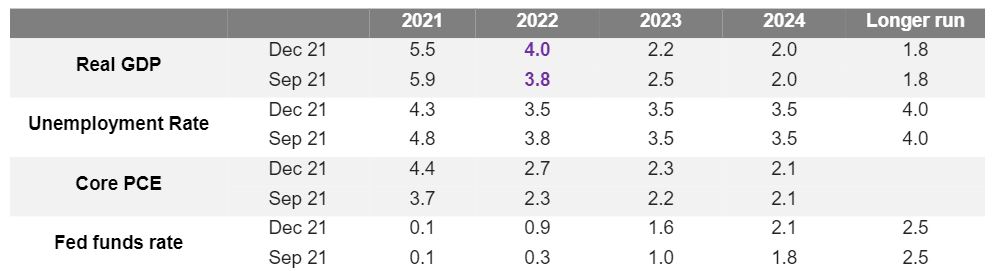

The refreshed dot plot which displays the 18 individual Fed members’ projections for interest rate hikes in the future, now shows three rate hikes in 2022. This illustrates just how concerned the Fed has become about inflation in just the last three months. In the September dot plot, half of the Fed officials believed they wouldn’t have to hike rates at all until 2023. Further out, officials now also see three more hikes in 2023 and two hikes in 2024, bringing the fed funds rate to 2.1%.

Summary of Economic Projections as of September and December 2021 (%)

Source: Federal Reserve

Upgraded GDP and inflation forecasts for 2022 suggest that the Fed feels the economy can weather the ongoing Omicron storm and Powell commented that Americans are increasingly learning to live with each new wave of Covid.

In a nutshell, with inflation elevated and the labour market making rapid progress, the Fed is preparing for a faster drawdown in asset purchases and for tighter policy next year. While the Fed adopted a hawkish tone, equity markets reacted positively as it was perceived as being less hawkish than feared, closing down what is probably the last obstacle for market participants to prepare for Christmas and new year celebrations. The posturing also brings reassurance that the Fed is moving to curb surging inflation.

The bad news for those looking to replace their Christmas jumper is that monetary policy kicks in with a lag. In the traditional CPI basket, apparel costs were up 5% YoY in November, and, if we look at online inflation tracked by Adobe, apparel costs rose +17.3% YoY (!) over the month.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

May 22, 2026

Weekly Investment Insights

Written as of 22 May 2026 All information is provided for informational purposes only and does not constitute investment advice or a recommendation. SpaceX...

May 19, 2026

BILBoardBILBoard May 2026 – Running on fumes

Based on the Asset Allocation Committee on May 5 2026 The conflict in the Middle East is now well into its third month, with traffic...

May 18, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Last week, US President Donald Trump travelled to China to meet President Xi Jinping to discuss trade, technology restrictions, global tensions, and potential...

May 11, 2026

NewsThe market closes the door on Fed rat...

Expectations for monetary policy easing by the US Federal Reserve (Fed) have shifted significantly since the start of the year. The conflict in the Middle...

May 11, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Oil prices rose again over the weekend as Washington and Tehran failed to come to an agreement to end the war in the...