BIL INVESTMENT INSIGHTS

Written on March 12 2026

After a weak 2025, when global supply far exceeded demand, oil markets have been thrown into turmoil as the conflict in the Middle East has halted crude and Liquified Natural Gas (LNG) flows through the Strait of Hormuz. About 20% of the world’s oil and LNG normally flow through this passage, which is now effectively blocked under the threat of Iranian attacks. With around 20 million barrels per day of crude and refined products removed from circulation, Brent spiked to $119.50 per barrel last weekend, now hovering at around $98 at the time of writing, up approximately 37% since before the conflict began. Dutch TTF, the European benchmark for natural gas, prices have also surged by around 65%.

Financial markets have reacted strongly. With memories of the 2022 energy crisis, when Russia’s invasion of Ukraine sent energy prices soaring and caused both bonds and equities to fall together, fresh in mind. Like in 2022, diversification has failed to offer protection, as both asset classes posted steep losses in response to the conflict. The jump in oil prices reflects investors’ fear that this conflict could trigger a structural global supply shock, potentially delaying or even reversing monetary easing as central banks confront renewed inflation pressures.

But compared to 2022, the global energy landscape looks quite different and economies are more prepared for such supply disruptions, even if the ultimate impact on prices will depend heavily on how long the conflict persists. The 2022 crisis was largely European and focused on pipeline gas, while today’s disruptions are global and affect both oil and LNG shipping routes. If the conflict drags on, the disruption could have a significant effect on global energy markets and economies. While we cannot predict when the conflict will be resolved, it is interesting to see how much the global energy situation has changed in four years, especially in Europe and the US.

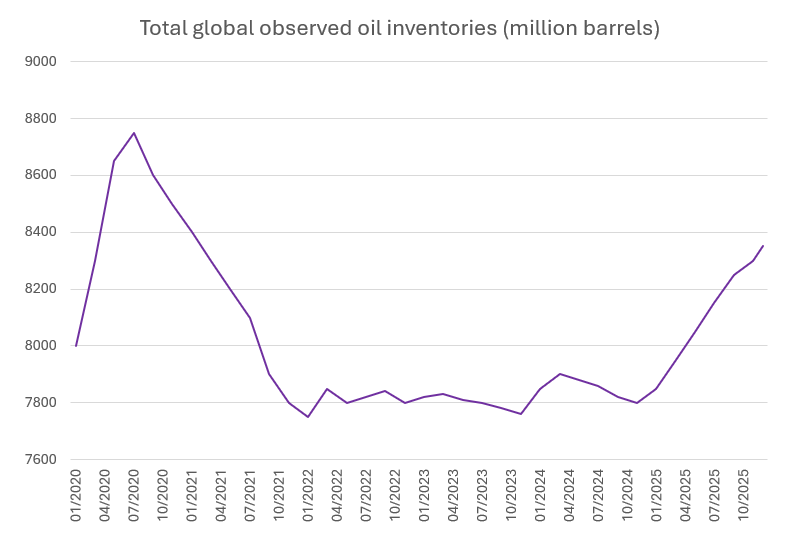

A different global picture

Global oil inventories rose above 8.2 billion barrels in 2025, the highest level since 2021, providing an important buffer. International Energy Agency member countries collectively hold more than 1.2 billion barrels of public emergency oil stocks, and the agency this week announced a record release of 400 million barrels to mitigate the impact of the disruption as attacks continue to target shipping and energy infrastructure.

Source: IEA, BIL

China, the world’s largest oil importer, has also built an estimated 120 days’ worth of strategic reserves, giving it flexibility to release crude if needed. Although it continues to buy oil, largely turning to discounted Russian barrels, it has significant leeway should the conflict continue over a prolonged period.

Meanwhile, the structure of global energy supply has shifted dramatically. The US became the world’s largest LNG exporter in 2023, overtaking Qatar and Australia, aided by Europe’s pivot away from Russian gas. In 2025, US shale production hit record levels, and the country became the first to export more than 100 million metric tons of LNG in a single year.

The coordinated release of strategic oil reserves by the IEA can temporarily bolster global supply, giving the US and other producers the time and flexibility needed to ramp up production and partially offset the loss of oil and LNG caused by the disruption in the Strait of Hormuz.

Winners and losers

For Europe, the energy shock is likely to be less devastating than in 2022, thanks to improved diversification. Russian gas dependence has fallen significantly, largely replaced by LNG, much of it coming from the United States. The EU now operates 33 LNG terminals, significantly expanding its import flexibility.

Still, Europe is not insulated. Any interruption of flows through the Strait of Hormuz immediately tightens global supply, forcing Europe into direct competition with Asia for available cargoes. This risk is compounded by the fact that Europe began 2026 with unusually low gas storage, at 30% full at the end of February, compared to 38% in 2025 and 62% in 2024. A prolonged disruption could impede the summer storage refill season, pushing up industrial energy costs and increasing the likelihood of inflation rising back above the European Central Bank (EBC)’s 2% target. Markets have already begun to price in the possibility of an ECB interest rate hike before year‑end in preparation of rising price pressures.

While Europe is better prepared than it was in 2022, the crisis highlights the ongoing challenge of achieving energy autonomy for the continent.

Across the Atlantic, the picture is markedly different. US consumers are already feeling the strain of higher gasoline prices, and inflation will likely rise in the near term. But unlike Europe, the United States also stands to benefit economically. Higher oil prices support increased shale production, capital spending, employment, and upstream investment. The US Energy Information Administration (EIA) expects US crude output to rise toward new records, and LNG exports remain elevated. While household spending will take a hit, the boost to GDP from higher production and export revenues could offset the drag.

Conclusion

The latest oil shock has rattled markets and revived memories of the 2022 energy crisis. While a lot has changed since 2022 and the global energy system is more diversified, more flexible, and better buffered than it was four years ago, we are still facing a significant energy supply disruption. Europe remains vulnerable, especially through LNG markets and low storage, but it is no longer facing an existential supply crisis. The United States, a net energy exporter, is positioned to benefit even as households feel the pinch.

Much will depend on how long the Strait of Hormuz remains disrupted. The longer the conflict continues, the greater the risk that temporary supply interruptions turn into structural losses, as damaged infrastructure and full storage tanks force production sites to shut down. The danger of this is not only the immediate loss of output - once these facilities go offline, restarting them can take far longer and prove more complex than many assume. If the crisis persists, the true test will be whether the resilience built since 2022 is enough to prevent a temporary shock from becoming a lasting fracture in the global energy system.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

March 30, 2026

Weekly Investment Insights

Kindly note that our Weekly Insights will pause over the upcoming bank holiday weekend. Market Snapshot The conflict in the Middle East has now extended...

March 23, 2026

Weekly InsightsWeekly Investment Insight

Equities and bonds extended declines last week as investors grew increasingly concerned about the prospect of a prolonged energy shock, following renewed attacks on key...

March 16, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot The ongoing conflict in the Middle East continued to push oil prices higher last week, with Brent crude briefly rising to $106 per...

March 10, 2026

BILBoardBILBoard March 2026 – Getting p...

As software stocks shed roughly $1 trillion in market value in February, investor attention swung toward capital‑intensive businesses with durable physical assets, captured by the...

March 9, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Global markets fell sharply on Friday as Middle East tensions escalated. With traffic through the Strait of Hormuz largely halted, Qatar’s state‑run energy...