BIL INVESTMENT INSIGHTS

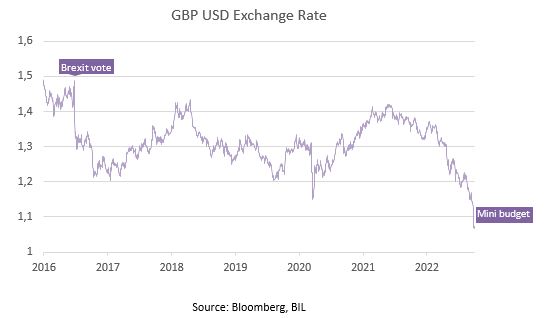

Globally, central banks are walking a very thin tightrope, attempting to contain soaring inflation without sending their respective economies into a tailspin. Nowhere does this look more precarious than in the UK, with the task complicated by the new government’s planned tax cuts and a plummeting pound.

While sterling had already been weakening against the US dollar over the past year, the unveiling of Chancellor Kwasi Kwarteng’s “mini budget” on September 23 was the clincher, sending the exchange rate to a record low.

The budget delivered a broad swathe of debt-funded tax cuts aimed at boosting growth and energising the economy. In reality, the cuts amounting to £45bn were perceived as potentially working at cross purposes to monetary policy, even by the IMF which urged the government to “re-evaluate” the plan, warning that the “untargeted” package might stoke inflation further.

As such, the economic plan put a huge dent in investor confidence, with some doubting whether the government would be able to fund these cuts against a backdrop of higher borrowing costs and ailing growth. The decline in confidence was visible not only sterling’s decline, but also in a rout in the UK government bond market, so severe the BoE had to step in to stave off a crash by pledging unlimited purchases of long-dated bonds and postponing quantitative tightening until October 31st (previously Oct. 3rd).

The BoE has been trying to orchestrate the softest possible landing for the economy as it attempts to cool inflation (which came in at 9.9% in August). This is a highly delicate task at the best of times, usually ending in recession (the BoE has said the UK might already be in one). Today, it is further complicated by the ongoing energy crunch in Europe, elevated utility bills and residual supply chain problems. While other central banks like the ECB have said that they will fine-tune their policy decisions with incoming data moving forward, the BoE has probably now been shoe-horned into hiking by even more than it would have initially to control the situation, increasing the chances of a deeper economic downturn.

The primary reason is that the plummeting pound is inflationary in itself, especially given that Britain imports about half of the goods it consumes. Following the announcement, BoE Chief Economist Pill said that “this will require a significant monetary policy response”, leading investors to price in a terminal rate above 6% next year; the current rate is 2.25%.

By hiking rates, the BoE can rein in demand and ultimately prices. By its own estimates, a 2 percentage point rise in interest rates could reduce aggregate spending by 1%. Higher rates would likely also take a toll on British manufacturing through higher input costs and exacerbate the cost of living crisis (by pushing up mortgage rates and debt servicing costs). This is of course not ideal for the UK economy but failing to act on inflation now could lead to even more severe consequences further down the line. So of course, the ultimate goal is to contain inflation with as few hikes as possible.

What the Bank of England cannot do is single-handedly entice foreign investors back into sterling and UK government bonds. Absent a U turn or at least some concessions from the Treasury on the budget, the BoE will probably continue to fight an uphill battle to decrease inflation, with a weak pound pushing against its efforts.

Analysts now expect a 100bp rate hike on Nov. 3, with risks skewed to a larger, earlier move.

For governments around the world, the lesson is clear: coordinated fiscal and monetary policy will be essential if we are to get inflation back under wraps.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

April 27, 2026

Weekly Investment Insights

Market Snapshot US equities continued their strong performance last week, with several major indices reaching record highs, as broadly positive economic data and upbeat earnings...

April 20, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot On Friday, equity markets celebrated the opening of the Strait of Hormuz to commercial shipping during the ceasefire. US equity markets posted strong...

April 13, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Last week, oil prices slumped and equities rallied after the US and Iran agreed a two-week ceasefire. However, hopes for de-escalation were quickly...

April 13, 2026

BILBoardBILBoard April 2026 – Through the noise

Based on the Asset Allocation Committee on March 31 2026 Geopolitical uncertainty took centre stage in March as the conflict in the Middle East extended...