BIL INVESTMENT INSIGHTS

Once installed in the Oval Office, Joe Biden disbursed a $1.9 trillion fiscal stimulus package. Titled the “American Rescue Plan”, it was aimed at changing the course of the pandemic and providing immediate relief to American households, using measures such as a new round of stimulus cheques. He ramped up the country’s vaccination drive and now, almost three million vaccine doses are administered in the US daily. Biden recently announced that every adult in the country will be eligible to be vaccinated by April 19th, instead of his original deadline of May 1st.

Next on Biden’s agenda is a package geared towards rebuilding the economy. Biden’s proposed infrastructure package, “The American Jobs Plan”, worth some $2.25 trillion, aims to create millions of jobs while “rebuilding America’s crumbling infrastructure” over a period of eight years. Moody's estimates that nearly 2.7 million jobs would be created by the plan.

The key areas for intended spending is broken down as follows:

$621bn for transport and infrastructure including:

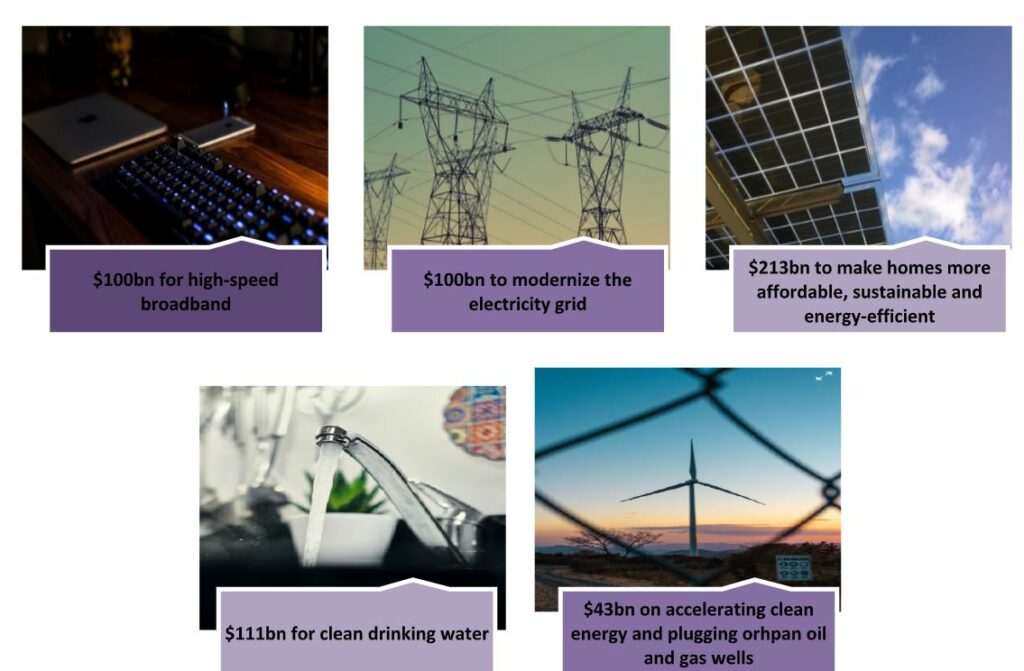

Over $650bn focused on improving quality of life including…

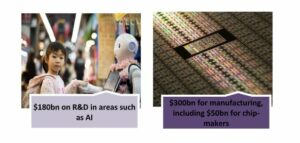

$480bn on manufacturing including:

In the fact sheet detailing the proposed Jobs plan, the Biden administration also notes that the health crisis has “unmasked the fragility” of the US caregiving infrastructure and “led to job losses and threatened economic security, eroding more than 30 years of progress in women’s labour force participation.” To address this, Biden wants to funnel $400 billion of the total $2.25 trillion towards improving access to quality, affordable home or community-based care. This would involve expanding a Medicaid program and would boost pay for care workers (who are largely female).

And Biden is not about to close the spending spigots there. According to reports, late-April, we might expect an additional spending proposal focused on social measures such as child tax credits, childcare, healthcare & education, which is expected to exceed $1tn. That spending would allegedly be paid for by tax increases on wealthy individuals.

How to pay for all this?

Together, the two proposed packages would total more than $3 trillion. With the US twin deficits already burgeoning (national debt stands at $28 trillion), the question is how to cover the costs? The proposals see the bill divided between corporations (roughly 2/3 of the total) and high income individuals (roughly 1/3), through higher taxes. For investors, corporate tax increases deserve greater consideration given their potential impact on markets.

As part of a tax overhaul, among other measures, the Biden administration intends to:

- Raise the domestic corporate tax rate from 21% to 28%

- Apply a global minimum corporate tax rate of 21% on overseas income

- Eliminate special tax credits for the fossil fuel industry

If Biden’s tax proposals are passed, it is estimated that they will pay for the infrastructure plan in full within the next 15 years and reduce deficits thereafter.

Will the Republicans warm to tax hikes?

The elephant in the room is the Republican one: While there has traditionally been bipartisan support for infrastructure investment, it is not clear if the Republicans will agree to increasing taxes – noises coming from Capitol Hill suggest not.

Prior to 2017, the domestic corporate tax rate was 35%, and had been since 1993. The GOP tax bill, which all Republicans voted for, slashed that rate from 35% to 21%. Biden now proposes to raise it to 28%.

Certain commentators have argued that raising taxes on American corporates could erode the international competitiveness of US firms and encourage them to relocate. Potentially countering this, Janet Yellen, the US Treasury secretary, has called on other countries to join Washington in setting a global minimum tax for firms. Yellen said she was working with G20 countries to agree on a global corporate minimum tax rate to end a “thirty-year race to the bottom on corporate tax rates”. On Tuesday, The European Commission backed Yellen’s call, but said its rate should be decided by the OECD.

The OECD has been drafting a two-pillar global taxation scheme for some time. The first pillar is intended to set a new regime for taxation of the largest multinationals (think tech giants like Google, Amazon and Facebook who make profits in countries where they do not hold a physical presence). To set the ball in motion with the OECD, the US has submitted its own proposal that would see big firms pay levies to national governments based on their sales in each country. The second pillar aims to establish a global minimum tax rate, which could apply to all companies, not just digital ones, so that governments do not compete with each other to attract large multinational firms. European Commission spokesman Dan Ferrie said that it is hoped all G20 finance ministers agree on both pillars by this July (however, this has typically been an area where consensus among EU member states has been elusive).

Quite notably, the CEO of Amazon, Jeff Bezos has come out and said he is in support of a corporate tax hike stating, "We support the Biden Administration's focus on making bold investments in American infrastructure."

What if the Republicans still aren’t convinced?

The Democrats have only a thin majority in both chambers of Congress and the plan will be subject to political wrangling and adjustments to garner support - even among Democrats such as Senator Joe Manchin who believes a 25% rate would be more appropriate.

Without Republican support, Democrats could resort to using the budget reconciliation mechanism - the same procedure that was used to enact the American Rescue Plan. On Monday, the Senate parliamentarian paved the way for the Democrats to do so, allowing Democrats in the evenly split 50-50 chamber to rely on a 51-vote threshold to advance some bills, thus shielding them from a filibuster that requires 60 votes to overcome. However, the reconciliation only allows bills that raise the deficit within a 10-year window. In its current form, the legislation would add to the deficit beyond a 10-year window and therefore, adjustments would be necessary.

What does this mean for investors?

While the plan is likely to be tweaked and watered down as it traverses through Congress, we still expect that a substantial package is on the horizon. Already, the US economy is thriving amid economic re-engagement and an unprecedented symbiosis of monetary and fiscal support; so much so that the IMF just upgraded its growth forecast for the US economy by 1.3% to 6.4%. The Fed expects 6.5%.

As such, we are overweight US equities, focusing on companies that are exposed to the reopening and recovery narrative, primarily in more cyclical sectors (industrials, materials and consumer discretionary). We also like utilities, a sector in which we cherry-pick the names that will benefit from Biden’s green-tinged infrastructure package and which allow us to participate in the secular megatrend of sustainability. We have also implemented a value-tilt in our US equity allocation. Despite recent rotations from Growth stocks to Value, they still look cheap compared to history and should take sap from the anticipated economic upswing and a gradual uptick in rates.

While markets have been busy baking in the benefits of infrastructure spending, attention is yet to focus on the impact of a potential corporate tax hike. The IT, healthcare and communications sectors were among the key beneficiaries when Trump slid the knife through corporate tax rates and indeed, they may be the most vulnerable to increases.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

July 27, 2026

Weekly Investment Insights

As anticipated in last week's note, the expiry of Section 122 tariff measures on 24 July was followed by the announcement of a new round...

July 17, 2026

BILBoardBILBoard July 2026 – A false dawn

Based on decisions taken at the July 6 Asset Allocation Committee Just a few weeks ago, it appeared that the worst of the Middle East...

July 17, 2026

Weekly InsightsWeekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 17, 2026

Weekly InsightsWeekly Investment Insights

Written 17 July, noon. Market Snapshot Markets faced competing headwinds this week: tensions in the Middle East and growing scrutiny of the AI theme, particularly...

July 13, 2026

Weekly InsightsWeekly Investment Insights

Geopolitical tensions returned to the forefront of financial markets last week. After tankers were reportedly targeted in the Strait of Hormuz, the US launched...