BIL INVESTMENT INSIGHTS

As summer approaches, some market participants might have recently contemplated the old investing adage “sell in May and go away.” This is the notion that investors should cash in their equity investments and take a summer break, re-entering the market around Halloween. In days gone by, some studies implied that stocks performed better between 31 October and May. We ran the numbers on a more recent dataset to see if the theory still holds up…

It is believed that the practice of selling shares in May originated in high society England, around 1700. The full version of the phrase is ‘sell in May and go away, come back on St. Leger’s Day’. This is a reference to the St. Leger Stakes horse race that is held every year mid-September. Back then, investors in London tended to sell their stocks before relocating to their country homes for the summer months where they would not be able to monitor them.

This, in turn, would have caused a market slump and then a subsequent lull in trading. With summer over, investors would return to the city and reopen their positions on the stock market, causing a lurch upwards in prices and a return of liquidity.

Fast-forwarding to the 21st century, summer still usually brings lower liquidity on markets. Long-run studies stretching as far back as 1928 have found that selling in May and coming back in October has not been a bad strategy on the S&P 500: The lowest average and median returns were prevalent in May through October. However, the results are slightly skewed by the fact that some of the worst days for performance in stock market history occurred in October, two of which were during the crash of 1929, and the other was the 1987 Black Monday crash.

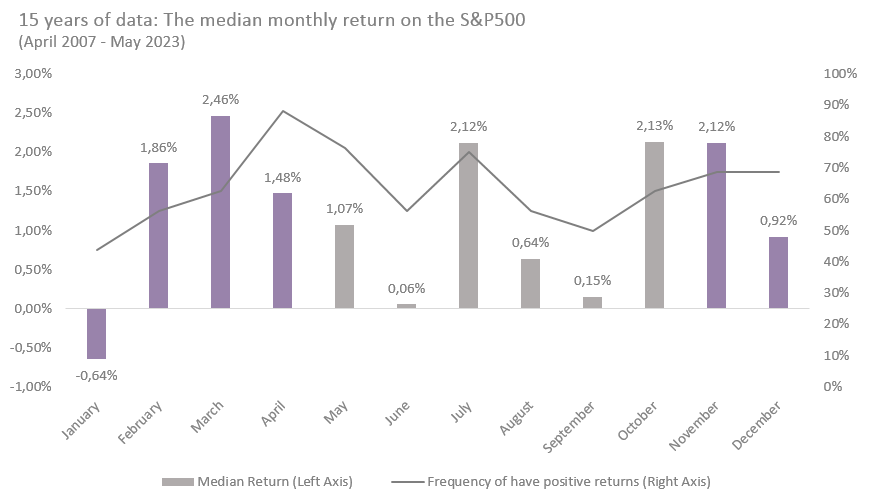

We ran the numbers on a more recent data set – going back fifteen years – to understand if it is still relevant. The results suggest that in modern times, at least on US markets, the adage may be more rhyme than reason.

Source: Bloomberg, BIL

Our findings show that during the period of interest, May – October, median returns were in fact positive, on average.

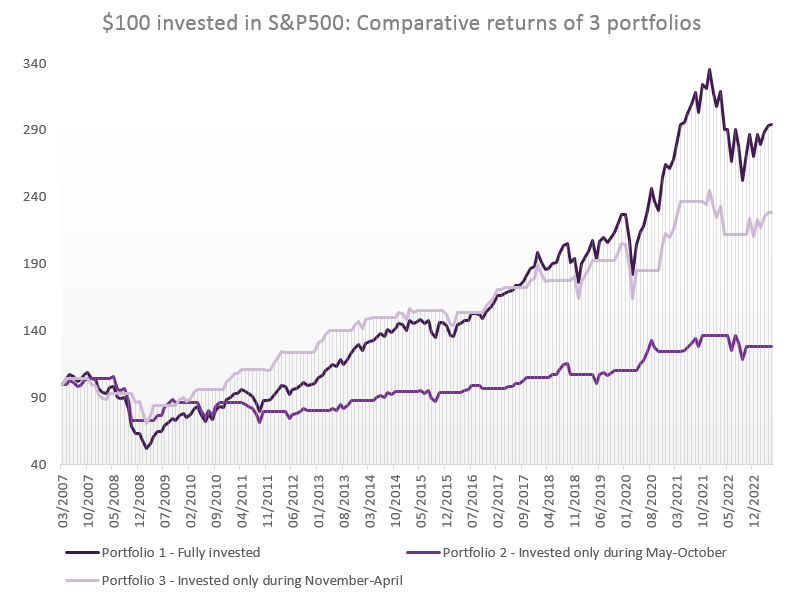

We then built three hypothetical portfolios: one that stayed fully invested ignoring the “sell in May” maxim, a second that invested from May-October each year and a third that invested from November-April each year. Each started out with a sum of $100.

Source: Bloomberg, BIL

Across the fifteen-year timespan, the portfolio that invested during the colder months clearly outperformed the ‘summer portfolio’. However, the portfolio that remained systematically invested throughout the year outperformed. Note that this is without considering the trading costs to exit and re-enter the market.

The risk of using portfolio 3 rather than portfolio 1 is to miss out on moments of market momentum. This was illustrated, for example, during the recovery from the pandemic shock in 2020 and 2021, when the May-October period performed particularly well.

It is notoriously difficult to time the market. Getting out at the right time before prices fall is hard enough, but then on top of that you have to reinvest before missing the recovery for the attempt to really pay off. Any time you switch into cash, you risk being on the sidelines when you could've been earning compound interest or when the market has some of its best days.

Moreover, trying to partake in seasonal effects is like gambling: As the small print on every financial document always says – past returns do not guarantee future performance. There's no assurance that a particular year will closely align with the long-term averages. Each year is unique with its own macro landscape, business cycle, and market environment that differentiates it from the past. Rigidly following calendar trading patterns without considering, for example, the ever-evolving earnings outlook and your unique investing goals and risk constraints, is not a wise strategy.

The summer effect might also be losing relevance in an increasingly digitalized world. Algorithmic trading now accounts for about 60-75% of overall trading volume in US equity markets. Machines don’t go on vacation!

As the movie Wall Street said – money never sleeps. We could also conclude that it doesn’t take summer holidays.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

May 22, 2026

Weekly Investment Insights

Written as of 22 May 2026 All information is provided for informational purposes only and does not constitute investment advice or a recommendation. SpaceX...

May 19, 2026

BILBoardBILBoard May 2026 – Running on fumes

Based on the Asset Allocation Committee on May 5 2026 The conflict in the Middle East is now well into its third month, with traffic...

May 18, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Last week, US President Donald Trump travelled to China to meet President Xi Jinping to discuss trade, technology restrictions, global tensions, and potential...

May 11, 2026

NewsThe market closes the door on Fed rat...

Expectations for monetary policy easing by the US Federal Reserve (Fed) have shifted significantly since the start of the year. The conflict in the Middle...

May 11, 2026

Weekly InsightsWeekly Investment Insights

Market Snapshot Oil prices rose again over the weekend as Washington and Tehran failed to come to an agreement to end the war in the...