BIL INVESTMENT INSIGHTS

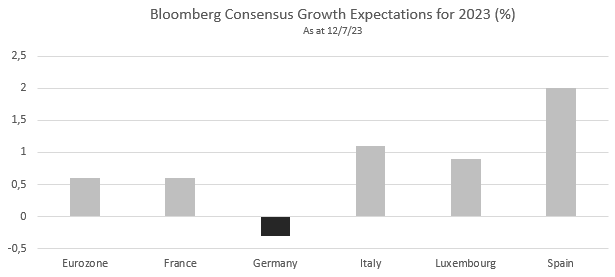

Germany, the fourth largest economy in the world and the leading economic power in the European Union, began 2023 in recession. Given pale full-year growth prospects relative to other countries on the continent, the idea that Germany is once again the “sick man of Europe” is in the airwaves. If this is the case, symptoms will not be contained within its borders…

In the late nineties, The Economist referred to Germany as “the sick man of Europe”. At the time, it was bearing the costs of reunification and grappling with high unemployment and weak domestic demand. After the turn of the Millennium, its economy underwent a rapid transformation. It went from being a laggard to becoming the locomotive that powered European growth. In 2022, it accounted for around one-quarter of the EU’s overall GDP.

The backbone of the German economy is its vast manufacturing sector, accounting for about one-fifth of of gross value-add. In very plain terms, Germany’s business model involved importing cheap raw materials and energy (the latter largely from Russia) and transforming them into world-class products.

Significant global demand for its goods means that around 40% of its GDP is attributable to exports. China has been Germany’s main trading partner for the seven years running, providing raw materials such as rare earth metals (needed for the transition to cleaner energy and transport) and serving as a important export market for German companies. The US is Germany’s second most important trading partner and a key buyer of Germany transportation equipment, machinery, chemicals and plastics. Over the past decade, the deep integration of the German industrial sector in international value chains has meant the country was a clear winner in the context of flourishing globalisation.

What’s weighing down the German economy?

Fast forward to today, Germany faces what is probably its biggest economic challenge since reunification. Slow-burning issues that were already weighing on the economy, such as rising protectionism and Germany’s diminishing competitiveness, have been accelerated by a double-blow of crises.

During the pandemic, Germany was naturally more exposed to global supply chain bottlenecks and before its manufacturing sector had time to fully recover, Russia invaded Ukraine. With an energy dependency ratio of 63% (versus an EU average of 57.5%), Germany was once again disproportionately impacted. Firms operating in the energy-intensive manufacturing sector could no longer rely on a steady flow of cheap gas from Russia and had to turn to volatile global energy markets.

Meanwhile, global trade conditions have soured. Following prolonged pandemic lockdowns, China’s economy is struggling to re-start, and the US is slowing as the Fed hikes rates to combat inflation.

But looking beyond the ups and downs of the economic cycle, the heydays of globalisation might be behind us. Protectionism is on the rise among friend and foes alike. Before the health crisis, the US imposed tariffs on European steel and aluminium, while more recently, the $369Bn Inflation Reduction Act, offers subsidies to companies willing to produce in the US, with emphasis on “Buy American”. In the East, China continues to chip away at Germany’s dominance in certain sectors as Beijing prioritises strategic sectors such as clean energy and transportation. To illustrate, the share of electric cars exported to Germany from China more than tripled in the first quarter of 2023, a worrying sign that its prized auto industry is struggling to keep pace as the combustion engine falls by the wayside. In the political sphere, calls are growing for Germany to reduce its “one-sided” dependency on China.

With its foreign trade model faltering, Germany can’t rely on domestic demand to support growth either. High inflation, rising interest rates and an erosion of real wages are taking their toll on domestic consumption, which fell 1.2% QoQ in Q1.

Then of course, the conversation wouldn’t be complete without mentioning the structural issues that hang over much of the old continent. Germany’s population is ageing. It needs to bring in 400,000 skilled foreign workers a year (far more than it has as of late) to offset this. It also lags behind in terms of digitalisation, with no FAANG equivalents to lead the charge as the fourth industrial revolution gets underway.

In some ways Germany has been a victim of its own success, leaning excessively on a model that has quite quickly become aged. Times are changing fast, and Germany will need to quickly reorient itself.

Germany’s struggles have implications for Europe

The fact that Germany’s business cycle is not synchronised with that of the rest of the Eurozone could be problematic for the ECB as it tries to set the optimal monetary policy stance, raising the risk of a policy misstep. Its economic significance also means that any prolonged downturn will be felt beyond its borders. Germany is the largest consumer market in the European Union with a population of 82.4 million. The list of European Union countries that count Germany as their No.1 trading partner is long. It includes France, Italy, the Netherlands, Belgium, Poland, Slovakia and… Luxembourg.

With 27% of the Grand Duchy’s total foreign trade taking place with Germany, if it does become the “sick man of Europe” once more, Luxembourg will most likely catch a cold.

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

June 19, 2026

Weekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...

June 16, 2026

BILBoardBILBoard Mid-Year 2026 – In sea...

Sunday, 21 June marks the official start of summer here in the northern hemisphere. Yet, after an unseasonably warm spring, conditions have turned cooler and...

June 15, 2026

Weekly InsightsWeekly Investment Insights

Written as of 15 June, After a volatile week, major US equity indices ended higher on Friday, supported by growing optimism around a potential...

June 5, 2026

Weekly InsightsWeekly Investment Insights

Written as at 5 June 2026 The record-breaking streak among chipmakers paused on Thursday after the outlook from a prominent player cast some doubt...

June 1, 2026

Weekly InsightsWeekly Investment Insights

Written as of 1 June 2026 US stock indices recorded new highs last week with investor optimism around AI serving as the driving force....