BIL INVESTMENT INSIGHTS

Global economic growth has slowed considerably throughout 2019 on the back of US-China trade tensions, with powerhouses like Germany skirting recession. Recently, with easier central bank policies starting to take effect, we have seen some stabilisation on the macro front and now, opinion is split between two central scenarios for 2020: will the global economy continue flatlining, or is this an inflection point where growth makes a comeback?

Throughout the slowdown, the manufacturing sector has

been the Achilles’ heel, while consumer spending – underpinned by robust labour

markets – has been the saving grace. While the latter remains intact, PMI data suggests

that manufacturing activity has finally found a floor, and has even started to

rebound, predominantly in emerging markets.

In the US, the manufacturing PMI also recently inched up from 51.1 to 51.3 (readings above 50 suggest expansion). It is true that the latest batch of industrial production data disappointed (falling 0.8%), but it is worth noting that the bulk of this was due to disruption in the auto sector amidst the General Motors strike, which saw some 48,000 employees out of the workforce for 40 days. Another positive is the fact that new export orders are back above the 50 level, which helped drive the slight moderation in ISM manufacturing data for October.

In Europe, the

situation looks marginally better than it did a month ago, but we are not yet

out of the woods. Industrial production data offered a little optimism,

expanding for the second month in a row in September, supported by domestic

demand. Further still, despite flirting with recession, business morale in

Germany rose to 95 as measured by the Ifo survey, pointing to Q4 growth of 0.2%

– again driven by domestic demand. However, the problem is that the weakness in

manufacturing may have already bled into the service sector. So while the

eurozone seems to have avoided freefalling growth, the danger to the economy

has not yet been averted, and for the export-oriented economy much hangs on a

US-China trade deal.

In most major economies, financial conditions remain

favourable and inflation is in check, while central banks remain accommodative:

the ECB is firing on all cylinders, whereas the Fed is on a hiatus after three

rate cuts, albeit leaving the door open to further stimulus if warranted. The

People’s Bank of China is also tweaking policy quite actively as it fine-tunes its pro-growth policy. Such

an environment should indeed support further extension of the cycle, especially

with the risks of a full-blown trade war and a no-deal Brexit dimming.

However, if trade talks were to suddenly take a U-turn,

things could quickly turn pear-shaped on the macro front. As it stands, things

seem to be moving in the right direction, with the most recent news coming from

US national security adviser Robert O’Brien, who opined that an initial trade

agreement with China is still possible by year-end.

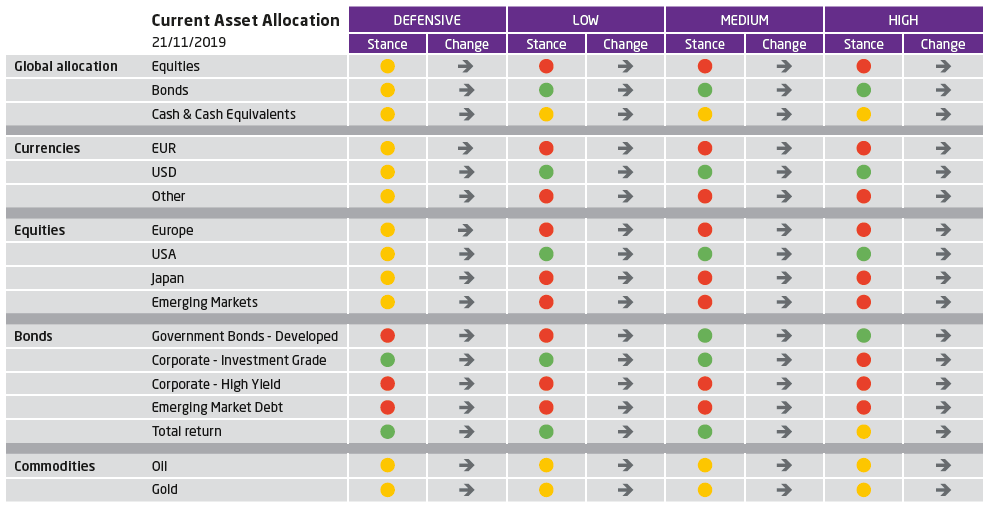

Equities

We have kept our equity exposure slightly underweight.

Although Q3 earnings surpassed expectations (a short-term market booster),

earnings growth on the whole has been essentially non-existent in both the US

and Europe. Analyst earnings expectations for next year are still quite lofty

and will be difficult to beat should we not see a marked improvement in the

macro landscape. If this materialises, stock markets have the stamina to reach

new highs. But this is quite a big ‘if’ and, in the meantime, investors seem to

have over-extrapolated the stabilisation in PMIs to conclude that PMIs are

headed upwards. This not yet the case, and there is risk that at some point,

attention could turn back to cold, hard fundamentals.

For now, a new gust of risk-on sentiment has blown a

lot of capital from defensives into cyclicals. We prefer to remain sector-neutral,

bearing in mind that sentiment is capricious and can turn at any time.

Furthermore, defensives look better when you drill down into the fundamentals

and top analyst expectations for Q4 earnings.

On a global scale, we prefer growth stocks at a

reasonable price (GARP) and large-caps in order to contain volatility.

Regionally speaking, the US continues to be the place to be, despite being a

bit pricey. We are underweight on Europe (which has suffered the most

collateral damage from the US-China trade war) and emerging markets (analysts

are currently predicting 14% revenue growth in 2020, which is likely to be

revised downwards). Japan is faring well (again thanks to domestic consumption)

and we may reconsider our underweight position early in 2020.

Fixed Income

We have seen a steady climb in rates again, catalysed

by trade optimism and hopes that we have reached a bottom in macro data. Will

this trend continue? Our experts believe that asymmetry is still alive, with there

being a greater probability of higher rates by the end of next year than lower rates.

We are neutral on US Treasuries and underweight on core European government

bonds for the time being. While these instruments may offer little on a

standalone basis, they serve as a cushion against equity market volatility. We

are neutral on duration (benchmark duration is around 7 years), and are reluctant

to reduce this while the white noise of political risk persists.

With most European govies offering negative yields,

European investment grade corporates are still the sweet spot for investors –

especially with ECB buying providing an added buffer against volatility. The

central bank kicked off its CSPP with a bang, buying EUR 2.5bn in the first two

weeks of November – more than expected – and with such support we are happy to

remain overweight on this asset class. In terms of US IG, we are neutral.

Though Fed policy can be seen as credit-friendly, the fundamental picture is

mixed, with gross leverage trending upwards and interest coverage falling.

We are underweight on high yield debt, which is still

expensive on both sides of the Atlantic given the embedded risk. For the small

exposure we do have, we prefer subordinated financials. These have the

potential to continue performing if peripheral European economies continue to

bottom out, while also having lower coupon risk: most banks are operating well above

MDA (maximum distributable amount) levels, which require regulators to

automatically restrict distributions if a bank’s total capital falls below a

predefined level. We are neutral on emerging market debt with a preference for

hard currency sovereigns, which have better liquidity characteristics.

Overall, our global allocation, with a slight underweight on equities, reflects our view of slowing growth but no recession. We prefer to wait and see with regard to increasing risk in our portfolios; after all, economic data is yet to confirm the second coming of growth, and a bottoming out may be as good as it gets.

Change: Indicates the change in our exposure since the previous month’s asset allocation committee

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

June 19, 2026

Weekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...

June 16, 2026

BILBoardBILBoard Mid-Year 2026 – In sea...

Sunday, 21 June marks the official start of summer here in the northern hemisphere. Yet, after an unseasonably warm spring, conditions have turned cooler and...

June 15, 2026

Weekly InsightsWeekly Investment Insights

Written as of 15 June, After a volatile week, major US equity indices ended higher on Friday, supported by growing optimism around a potential...

June 5, 2026

Weekly InsightsWeekly Investment Insights

Written as at 5 June 2026 The record-breaking streak among chipmakers paused on Thursday after the outlook from a prominent player cast some doubt...

June 1, 2026

Weekly InsightsWeekly Investment Insights

Written as of 1 June 2026 US stock indices recorded new highs last week with investor optimism around AI serving as the driving force....