BIL INVESTMENT INSIGHTS

Much has

changed since our last BILBoard note. The Democratic candidate, Joe Biden, won

the US presidential election, but the “blue wave” that markets had anticipated

did not materialise. Despite being caught wrong-footed, they quickly adopted

the opinion that a divided Congress was in fact the most palatable scenario to

prevent policy veering too far to the left. November also brought hope on the

vaccine front with two candidates delivering efficacy rates of around 95% in

trials. There’s a long way to go until the eventual distribution of any

vaccine, but heady sentiment sent the S&P 500 and the Dow Jones to new

all-time highs, and acted as a catalyst for a brief but violent rotation from

growth into value. However, optimism about the future and a solution to the

health crisis must be balanced against the reality of the here and now, with soaring

infection levels on both sides of the Atlantic inciting new restrictive measures.

Macro

The

epidemiological situation is showing up in the macro data, but not to the

extent that we need to adjust our base case. Thanks to monetary and fiscal

support, we still believe that an economic recovery through 2021 is on the menu,

with the wealth lost during the crisis recuperated in 2022.

In the US,

the recovery has been stronger than expected. On the corporate side, rising

industrial output, capacity utilisation and durable goods orders all point to a

pick-up, while the ISM survey indicates that both manufacturing and services

are in expansionary territory. This bodes well for the labour market and already

in October, the unemployment rate fell by a full percentage point to 6.9%.

Despite this, consumer sentiment has been dampened by rising case numbers. An extra helping of fiscal stimulus is due, but it is just hoped

that President Trump’s last months in the Oval Office go past without any show stoppers.

In Europe, third quarter GDP growth jumped more than expected (+12.7%), thanks to the removal of movement restrictions. But said restrictions are now being rolled out again, leaving the continent teetering on the edge of a double-dip scenario. It does not help that the much-awaited fiscal stimulus package is on the backburner after being blocked by Hungary and Poland, leaving the ECB in the driving seat when it comes to supporting the economy for now. The central bank is expected to expand measures at its December meeting but ultimately, there is little they can do to embolden consumers apart from alleviating the pressure of existing debt. In this area, there is a clear need for fiscal support.

The Chinese

economy is enjoying a clear V-shaped bounce-back, expanding 4.9% in Q3 due to a

faster than expected recovery in exports and retail sales. Both the

manufacturing and service sectors showed strong growth in October, and PMI data

points to continued expansion, helped by targeted fiscal support.

Fixed Income

The vaccine

breakthrough pushed rates higher, but increases are tempered by central bank

largesse, as well as concerns over mounting COVID-19 cases. The hunt for yield

is on again, and with $16 trillion of debt offering negative yields, investors

are venturing down the quality curve in search of income. It is crucial for

investors to remain selective in order to successfully navigate the risk/return

trade-off.

In the sovereign space, risk-free rates in the US are slowly rising with the economy showing dynamism, while European yields have retreated as the continent battles with its old demons of low growth and no inflation. Low and negative yields make govies the proverbial Brussels sprouts of a balanced portfolio, standard fare but not very appetizing. We are particularly cautious on duration in the US where there is the potential for a slow uptick in yields.

We continue

to prefer investment grade (IG) corporate bonds which are supported by

improving fundamentals. After months of sideways trading, vaccine news allowed

spreads to break through previous resistance levels, even falling below the 100

bps level in Europe. The IG market is supported by central banks for the time

being, and in Europe this is likely to persist into 2021. In the US, the IG bond

market is already standing on its own two feet, with the Fed only using a

fraction of its firepower. When it became apparent that the Fed will not continue

with corporate bond purchases in 2021, markets reacted calmly: corporates will

of course still receive indirect support from the Fed’s purchases in the

Treasury space.

High-yield

bonds have also broken through resistance levels and the yield on the US HY segment

hit an all-time low of 4.56% this month. With flows strong, default levels remaining

contained and the potential for some spread compression (predominantly between

BBB and BB), we are taking a selective approach to this asset class. The HY

buffet has a wide variety of companies—some are decent, whereas others are a

no-go area. Careful selection is key, especially with Moody’s forecasting that

defaults will not peak until March.

We continue

to favour emerging market corporate bonds over emerging market sovereigns due

to their volatility profile and shorter duration characteristics.

Equities

Overall, we

are positive on equities. On the heels of the Q3 earnings season, which was

much better than analysts had feared in both the US and Europe, analyst

revisions for earnings growth over the next 12 months have been turning

positivein all regions except Japan. We still prefer the US (home of

quality growth names and stay-at-home beneficiaries) and China (due to strong

domestic growth).

The scenario of interest rates remaining lower for

longer still favours the quality/growth style, and this remains our preference.

However, as we witnessed in November, relief rallies often come hand-in-hand

with short-lived but violent style rotations. While we do not believe that the

current environment is conducive to the prolonged outperformance of value

stocks, portfolios require protection against any temporary shifts in sentiment

that may arise. In order to achieve this, we have introduced some cyclicality

via our sector bets, primarily by reducing exposure to Consumer Staples in

favour of Industrials.

Industrials is a mid-to-late cycle sector that offers

a play on rising PMIs. It will be a key beneficiary of large-scale fiscal

stimulus programmes in both the US and Europe. We have also become more

positive on Materials. China’s recovery and a pick-up in industrial

activity are among the factors driving the sector’s strong earnings revisions,

as well as rises in commodity prices. While the sector looks expensive at first

glance, this is largely due to high valuations in the Chemicals subsector, and

value can still be found elsewhere.

While the above sectors bring a flavour of value, we balance this with strong growth sectors which we believe still have room to run, especially while the pandemic remains rampant. These safer plays are: IT, a sector with resilient earnings growth, strong cash flow generation and healthy balance sheets that benefits from both the stay-at-home theme and the structural shift towards digitalisation; Healthcare, a defensive sector that has gained impetus from the pandemic; and Utilities,another defensive sector that is benefitting—and will continue to benefit—from the global focus on renewables and clean energy.

...

It is not yet time to position portfolios for a value renaissance. However, as the economic recovery progresses, stocks that do not have the pizzazz of tech highflyers could start to make a comeback—especially when new fiscal stimulus packages begin to percolate through into the real economy next year. For the time being, we keep a main course of quality/ growth stocks, accompanied by a small helping of value stocks as some kind of amuse-bouche that will help investors stomach any temporary style rotations.

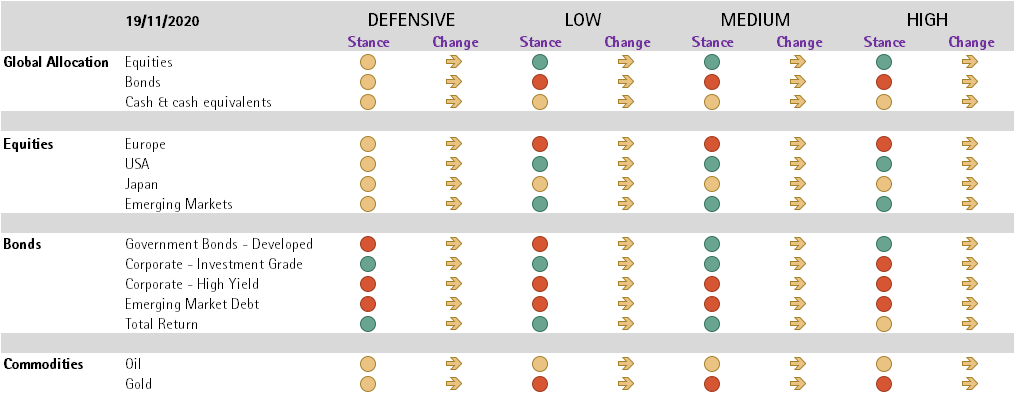

Change: Indicates the change in our exposure since the previous month’s asset allocation committee

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

June 19, 2026

Weekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...

June 16, 2026

BILBoardBILBoard Mid-Year 2026 – In sea...

Sunday, 21 June marks the official start of summer here in the northern hemisphere. Yet, after an unseasonably warm spring, conditions have turned cooler and...

June 15, 2026

Weekly InsightsWeekly Investment Insights

Written as of 15 June, After a volatile week, major US equity indices ended higher on Friday, supported by growing optimism around a potential...

June 5, 2026

Weekly InsightsWeekly Investment Insights

Written as at 5 June 2026 The record-breaking streak among chipmakers paused on Thursday after the outlook from a prominent player cast some doubt...

June 1, 2026

Weekly InsightsWeekly Investment Insights

Written as of 1 June 2026 US stock indices recorded new highs last week with investor optimism around AI serving as the driving force....